At some point, you’ve probably heard the saying: “Yesterday was the best time to buy a home, but the next best time is today.”

That’s because homeownership is about the long game – and home prices typically rise over time. So, while you may be holding out for prices to fall or rates to improve, you should know that trying to time the market rarely works.

Here’s what most buyers don’t always think about: the longer you wait, the more buying could cost you. And you deserve to understand why.

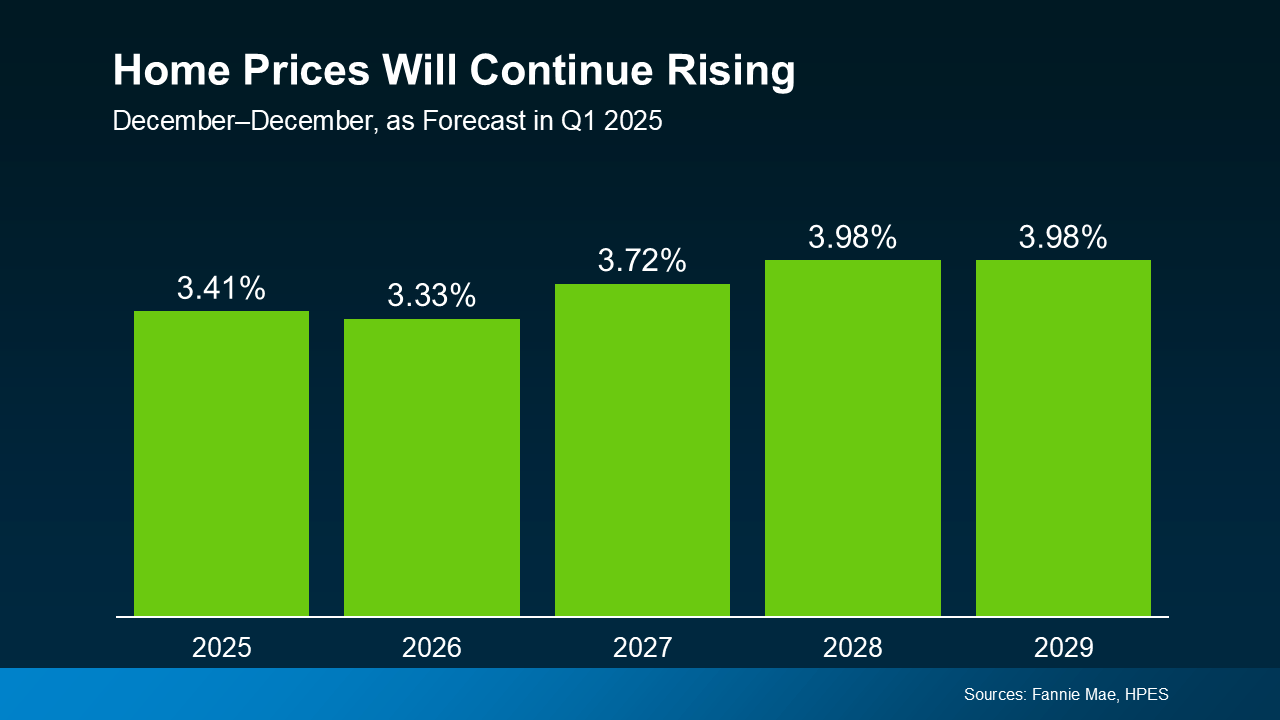

Forecasts Say Prices Will Keep Climbing

Each quarter, over 100 housing market experts weigh in for the Home Price Expectations Survey from Fannie Mae, and they consistently agree on one thing: nationally, home prices are expected to rise through at least 2029.

Yes, the sharp price increases are behind us, but experts project a steady, healthy, and sustainable increase of 3-4% per year going forward. And while this will vary by local market from year to year, the good news is, this is a much more normal pace – a welcome sign for the housing market and hopeful buyers (see graph below):

And even in markets experiencing more modest price growth or slight short-term declines, the long game of homeownership wins over time.

So, here’s what to keep in mind:

Next year’s home prices will be higher than this year’s. The longer you wait, the more the purchase price will go up.

Waiting for the perfect mortgage rate or a price drop may backfire. Even if rates dip slightly, projected home price growth could still make waiting more expensive overall.

Buying now means building equity sooner. When you play the long game of homeownership, your equity rewards you over time.

What You’ll Miss Out On

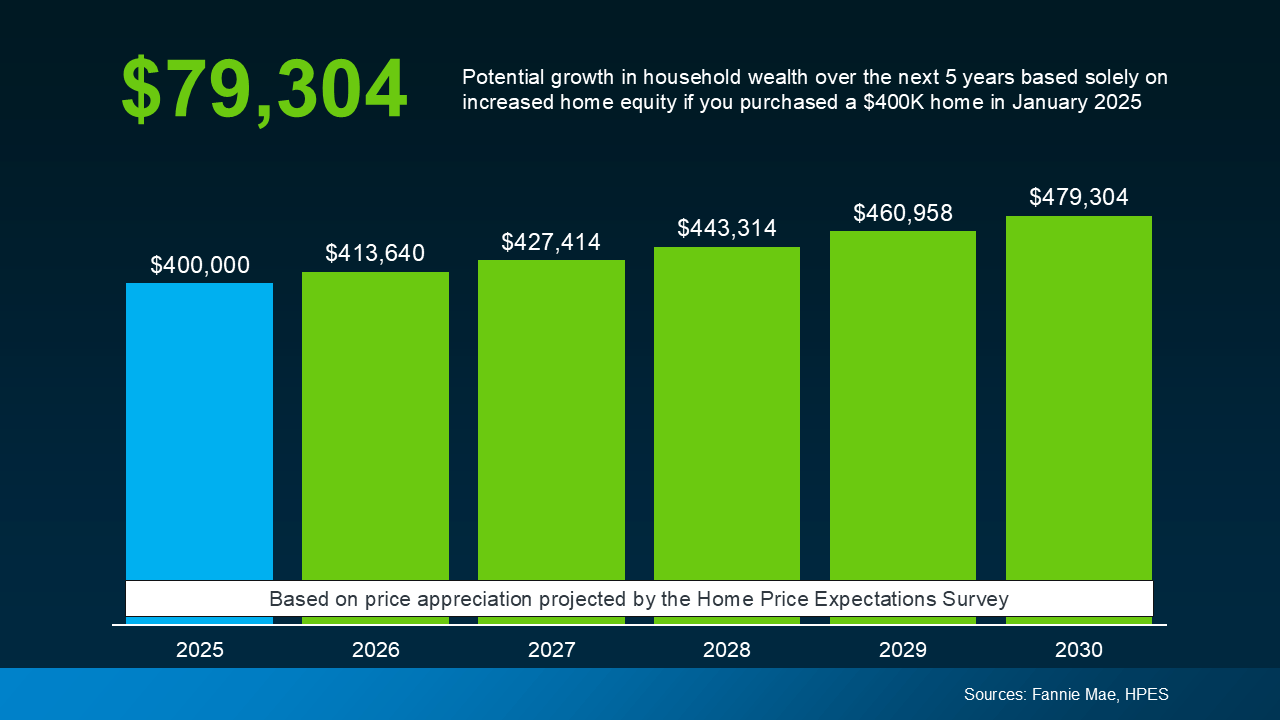

Let’s put real numbers into this equation, because it adds up quickly. Based on those expert projections, if you bought a typical $400,000 home in 2025, it could gain nearly $80,000 in value by 2030 (see graph below):

That’s a serious boost to your future wealth – and why your friends and family who already bought a home are so glad they did. Time in the market matters.

So, the question isn’t: should I wait? It’s really: can I afford to buy now? Because if you can stretch a little or you’re willing to buy something a bit smaller just to get your foot in the door, this is why it’ll be worth it.

Yes, today’s housing market has challenges, but there are ways to make it work, like exploring different neighborhoods, asking your lender about alternative financing, or tapping into down payment assistance programs.

The key is making a move when it makes sense for you, rather than waiting for a perfect scenario that may never arrive.

Bottom Line

Time in the Market Beats Timing the Market.

If you’re debating whether to buy now or wait, remember this: real estate rewards those who get in the market, not those who try to time it perfectly.

Want to take a look at what’s happening with prices in our local area? Whether you’re ready to buy now or just exploring your options, having a plan in place can set you up for long-term success.

What’s Your House Worth Now? The Answer May Surprise You

Let’s talk about something you might not check nearly as often as your bank account – and that’s how much your home is worth. But when it comes to your financial situation, it’s an important thing to remember. When’s the last time you had a professional show you the value of your home?

Think about it. For most people, your house is probably the biggest asset you have. And if you’ve owned your home for a few years (or longer), chances are it’s been quietly building wealth for you in the background. And honestly? You might be surprised by just how much.

What Is Home Equity?

This wealth you may not even realize you have comes in the form of home equity. Home equity is the difference between what your house is worth and what you still owe on your mortgage. It grows over time as home values rise and as you pay down your mortgage each month. Here’s an example to help you really understand how this works.

Let’s say your house is now worth $500,000, and you have $200,000 left to pay off on your loan. That means you have $300,000 in equity. And most homeowners are sitting on some pretty significant equity right now.

According to Cotality (formerly CoreLogic), the average homeowner with a mortgage has about $311,000 in equity.

Why You Probably Have More Than You Think

Here are the two main reasons homeowners like you have record amounts of equity right now:

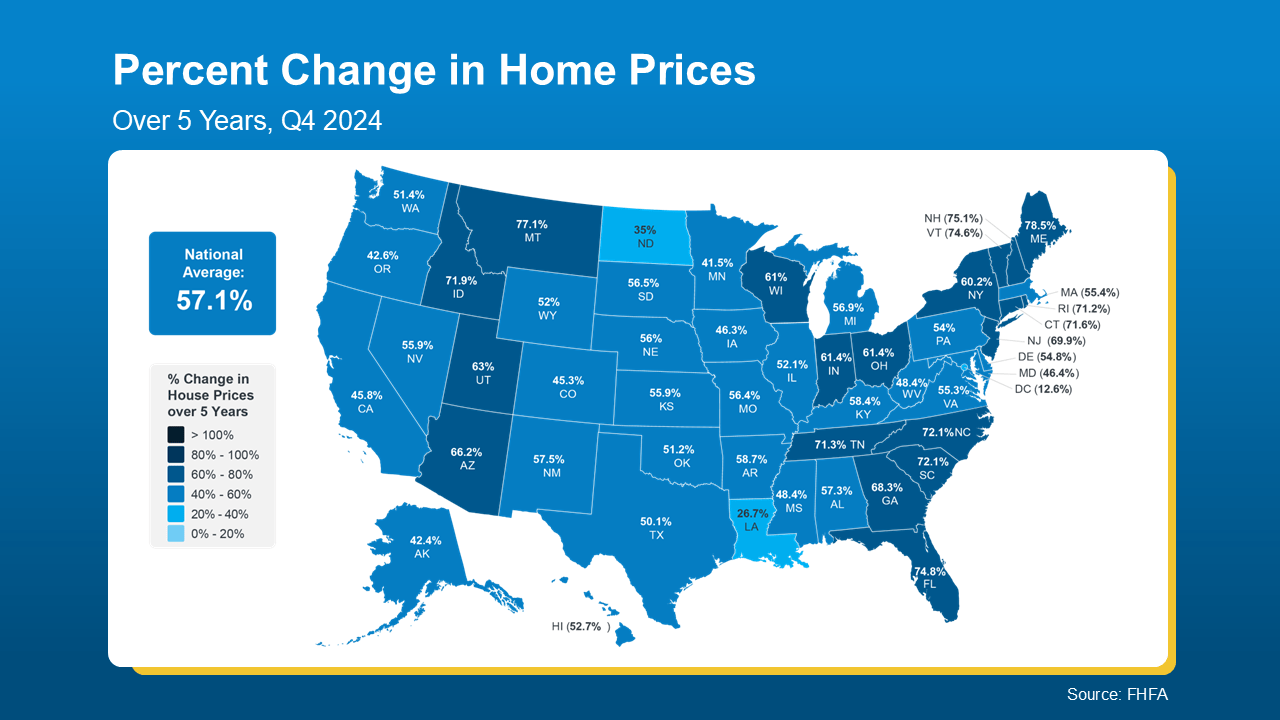

1. Significant Home Price Growth.According to the Federal Housing Finance Agency (FHFA), home prices have jumped by more than 57% nationwide over the last five years (see map below):

And if you purchased your home a few years ago (or more), this means your house is likely worth much more now than when you first bought it, thanks to how much prices have climbed lately.

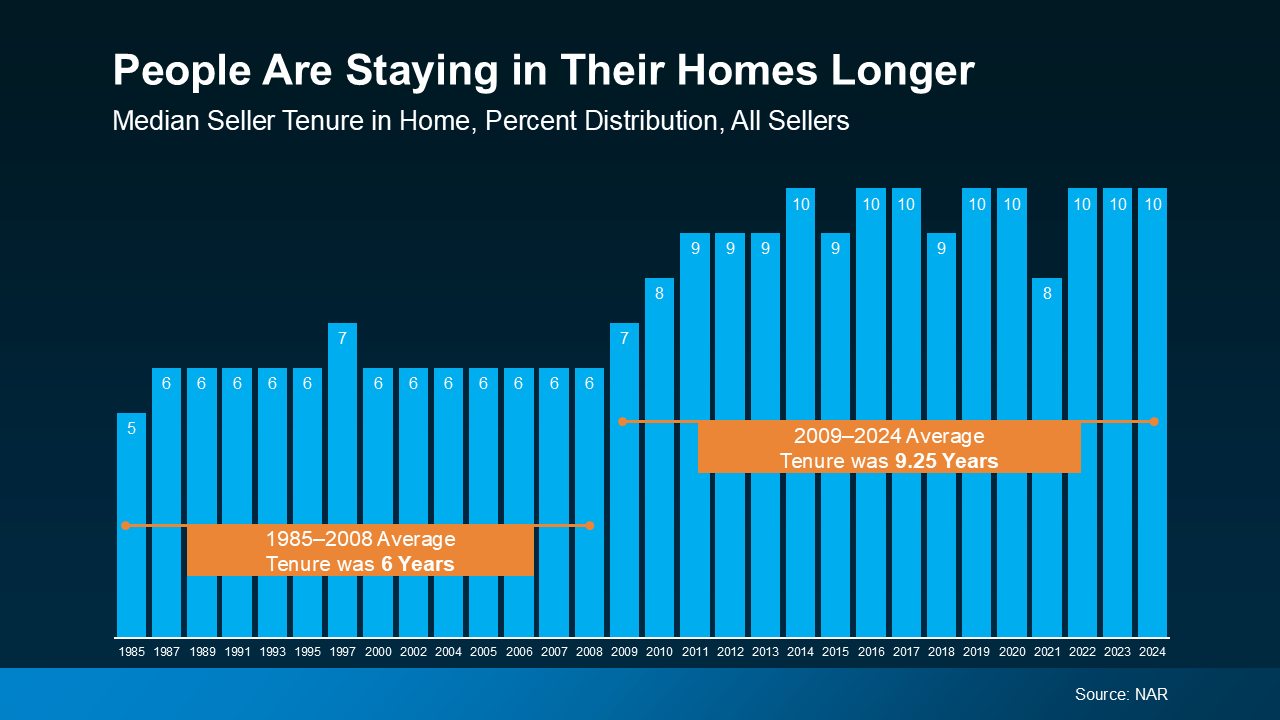

2. People Are Living in Their Homes Longer.Data from the National Association of Realtors (NAR), shows the average homeowner stays in their home for about 10 years now (see graph below):

That’s longer than it used to be. And over that decade? You’ve built equity just by making your mortgage payments and riding the wave of rising home values.

So, if you’re one of those people who’s been in their home for that long, here’s how much the behind-the-scenes price growth has helped you out. According to NAR:

“Over the past decade, the typical homeowner has accumulated $201,600 in wealth solely from price appreciation.”

What Could You Actually Do with That Equity?

Remember, your house might be your biggest financial asset – and, if you’re smart about how you leverage your equity, it could open up some exciting opportunities for your future.

Use it to help buy your next home. Your equity could help you cover the down payment on your next home. In some cases, it might even mean you can buy your next house in all cash.

Renovate your current house to better suit your life now. And, if you’re strategic about your projects, they could add even more value to your home if you do sell later on.

Start the business you’ve always dreamed of. Your equity could be exactly what you need for startup costs, equipment, or marketing. And that could help increase your earning potential, so you’re getting yet another financial boost.

Bottom Line

Chances are, your house is worth a lot more than you realize. Whether you’re thinking about selling, upgrading, or simply want to understand your options, your equity isn’t just a number. It’s a tool.

If you sold your house and had significant equity to work with, what would you do with it? Let’s figure out how to turn your home’s value into your next big move.

Richard Iarossi, REALTOR®

Coldwell Banker Realty

1300 Main Chapel Way, Gambrills, MD 21054

443.995.9595 Cell

410-721-0103 Office

rich@richsellshomes.com

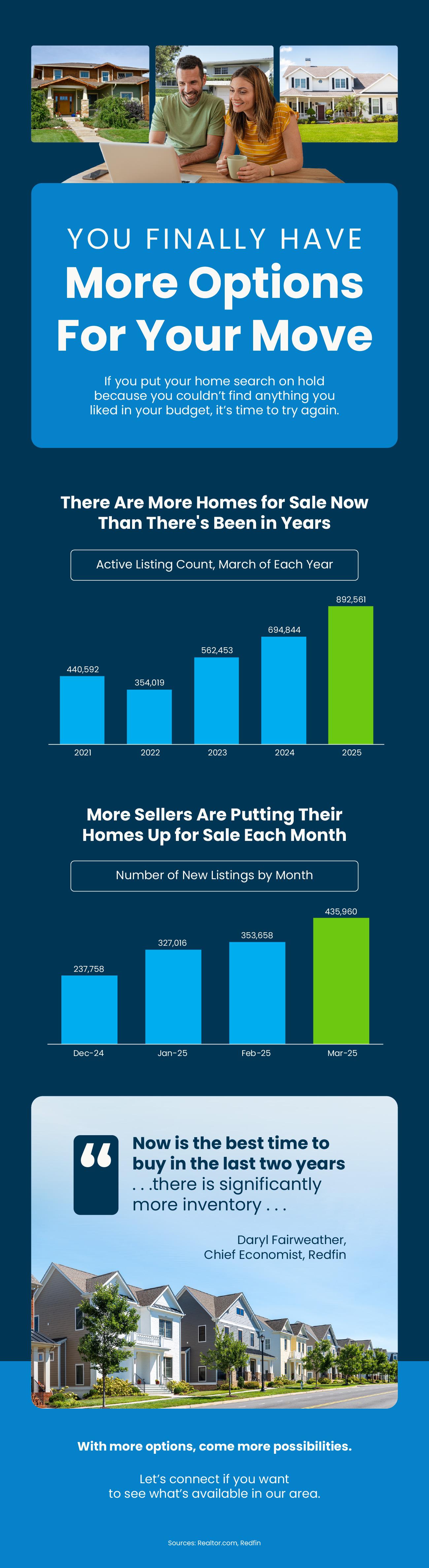

Paused Your Moving Plans? Here’s Why It Might Be Time To Hit Play Again

Last year, 70% of buyers abandoned their home search – and maybe you were one of them. It makes sense. Inventory was low, prices were high, and mortgage rates were up and down like a rollercoaster. All of that made it really hard to find a home you loved – and could afford.

But guess what? The market is shifting.

So, if you paused your moving plans in 2024, it might be time to hit play again. Here’s why.

More Inventory Opens Up More Options

Even if you could make the numbers work, the lack of available homes in recent years probably made it hard to come by something that fit your needs. But inventory is rising, which means you have more options now.

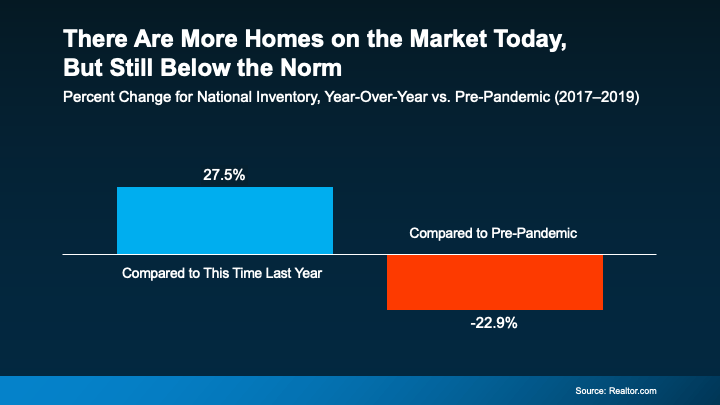

According to Realtor.com, inventory has jumped 27.5% since this time last year (see graph below):

So, if you were reluctant to list your house because you weren’t sure where you’d go if it sold, you have more choices than you did a year ago. That’s a big win.

Homes Are Staying on the Market Longer, Too

When the supply of homes for sale is low, they’re snatched up quickly because there just aren’t enough of them to go around. And a few years ago, that meant your house could sell overnight. While that’s not always a bad thing, if you’re planning a move and also need to find your next home, a slower pace isn’t the end of the world. In fact, it’s welcome relief.

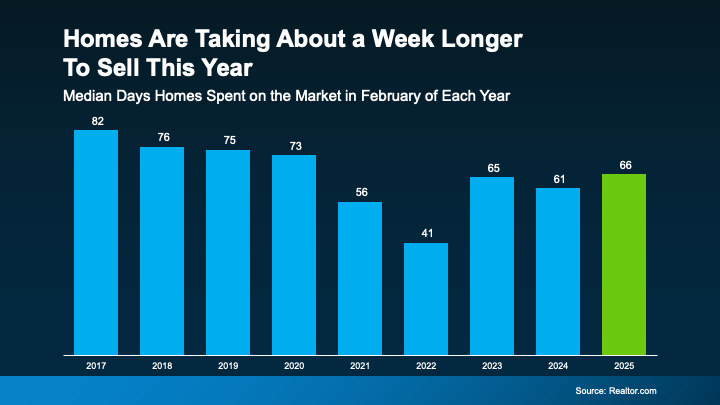

Now that inventory has grown, homes are staying on the market longer, meaning you don’t have to feel as rushed in the process (see graph below):

The latest data shows the typical time homes spent on the market went up by about 8% this year – that’s higher than we’ve seen since 2020, but still a faster pace than before the market ramped up. And it’s about a week longer than last year. Talk about a sweet spot for movers. It may seem like just a few days, but it gives you more flexibility and time to be thoughtful about your decisions. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, notes:

“There are more homes for sale than in the last few years, which means the market pace is a bit more manageable–with longer days on market–and many sellers are more flexible . . . Though buyers face still-high housing costs, they may find a bit more give in the market, which could give them more time to make a decision, even in the busy spring and summer months.”

And if you’re thinking – but wait – doesn’t that mean it will be harder to sell my house? Don’t worry. With inventory still almost 23% below the pre-pandemic norm, well-priced homes are selling, especially as more buyers step back into the game this season.

Bottom Line

With growing inventory, sellers who want to upgrade, downsize, or relocate have more choices. Plus, with less pressure to rush into an offer, it could be a great time to revisit your home search if you’ve put it on hold.

With more homes on the market and more time to make decisions, what else do you need to see in order to kickstart your home search again? Let’s talk about what’s happening in our local market right now.

Last year, 70% of buyers abandoned their home search – and maybe you were one of them. It makes sense. Inventory was low, prices were high, and mortgage rates were up and down like a rollercoaster. All of that made it really hard to find a home you loved – and could afford.

But guess what? The market is shifting.

So, if you paused your moving plans in 2024, it might be time to hit play again. Here’s why.

More Inventory Opens Up More Options

Even if you could make the numbers work, the lack of available homes in recent years probably made it hard to come by something that fit your needs. But inventory is rising, which means you have more options now.

According to Realtor.com, inventory has jumped 27.5% since this time last year (see graph below):

So, if you were reluctant to list your house because you weren’t sure where you’d go if it sold, you have more choices than you did a year ago. That’s a big win.

Homes Are Staying on the Market Longer, Too

When the supply of homes for sale is low, they’re snatched up quickly because there just aren’t enough of them to go around. And a few years ago, that meant your house could sell overnight. While that’s not always a bad thing, if you’re planning a move and also need to find your next home, a slower pace isn’t the end of the world. In fact, it’s welcome relief.

Now that inventory has grown, homes are staying on the market longer, meaning you don’t have to feel as rushed in the process (see graph below):

The latest data shows the typical time homes spent on the market went up by about 8% this year – that’s higher than we’ve seen since 2020, but still a faster pace than before the market ramped up. And it’s about a week longer than last year. Talk about a sweet spot for movers. It may seem like just a few days, but it gives you more flexibility and time to be thoughtful about your decisions. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, notes:

“There are more homes for sale than in the last few years, which means the market pace is a bit more manageable–with longer days on market–and many sellers are more flexible . . . Though buyers face still-high housing costs, they may find a bit more give in the market, which could give them more time to make a decision, even in the busy spring and summer months.”

And if you’re thinking – but wait – doesn’t that mean it will be harder to sell my house? Don’t worry. With inventory still almost 23% below the pre-pandemic norm, well-priced homes are selling, especially as more buyers step back into the game this season.

Bottom Line

With growing inventory, sellers who want to upgrade, downsize, or relocate have more choices. Plus, with less pressure to rush into an offer, it could be a great time to revisit your home search if you’ve put it on hold.

With more homes on the market and more time to make decisions, what else do you need to see in order to kickstart your home search again? Let’s talk about what’s happening in our local market right now.

Richard Iarossi, REALTOR

Coldwell Banker Realty

1300 Main Chapel Way, Gambrills, MD 21054

443.995.9595 Cell

410.721.0103 Office

rich@richsellshomes.comm

richsellshomes.com

Here’s What a Recession Could Mean for the Housing Market

Recession talk is all over the news, and the odds of a recession are rising this year. And that leaves people wondering what would happen to the housing market if we do go into a recession.

Let’s take a look at some historical data to show what’s happened in housing for each recession going all the way back to the 1980s.

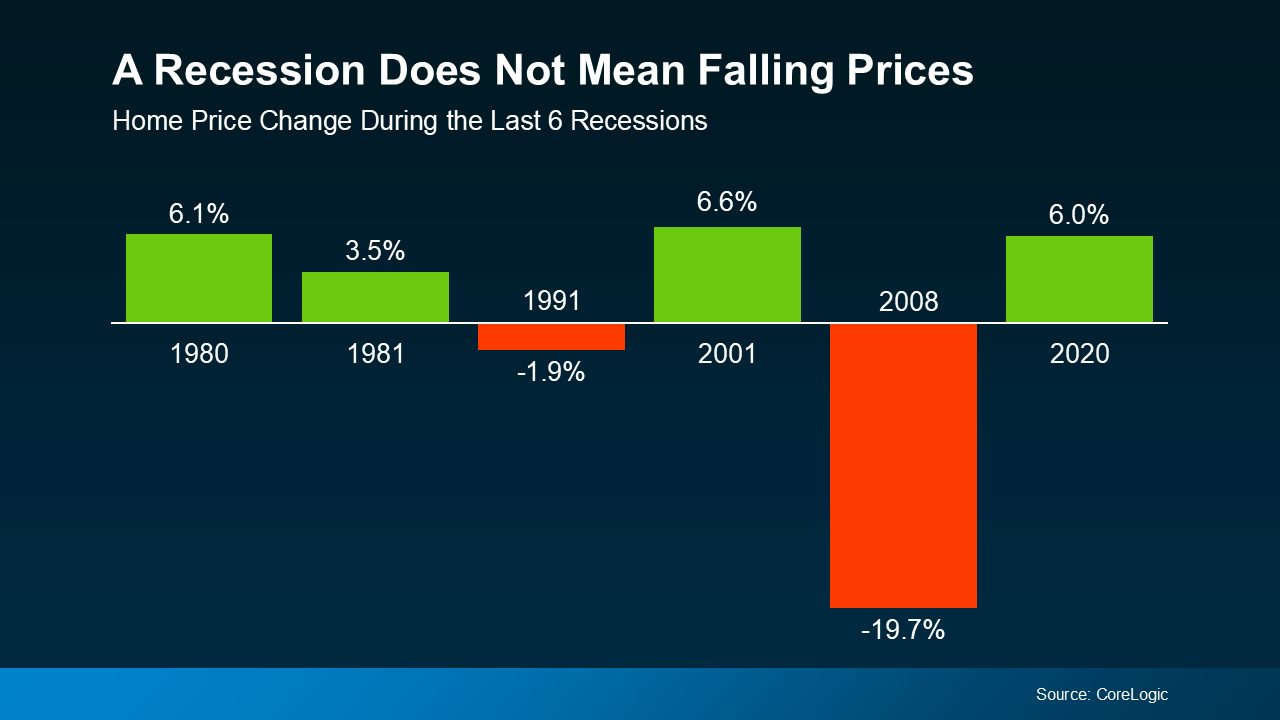

A Recession Doesn’t Mean Home Prices Will Fall

Many people think that if a recession hits, home prices will fall like they did in 2008. But that was an exception, not the rule. It was the only time we saw such a steep drop in prices. And it hasn’t happened since.

In fact, according to data from CoreLogic, in four of the last six recessions, home prices actually went up (see graph below):

So, if you’re thinking about buying or selling a home, don’t assume a recession will lead to a crash in home prices. The data simply doesn’t support that idea. Instead, home prices usually follow whatever trajectory they’re already on. And right now, nationally, home prices are still rising at a more normal pace.

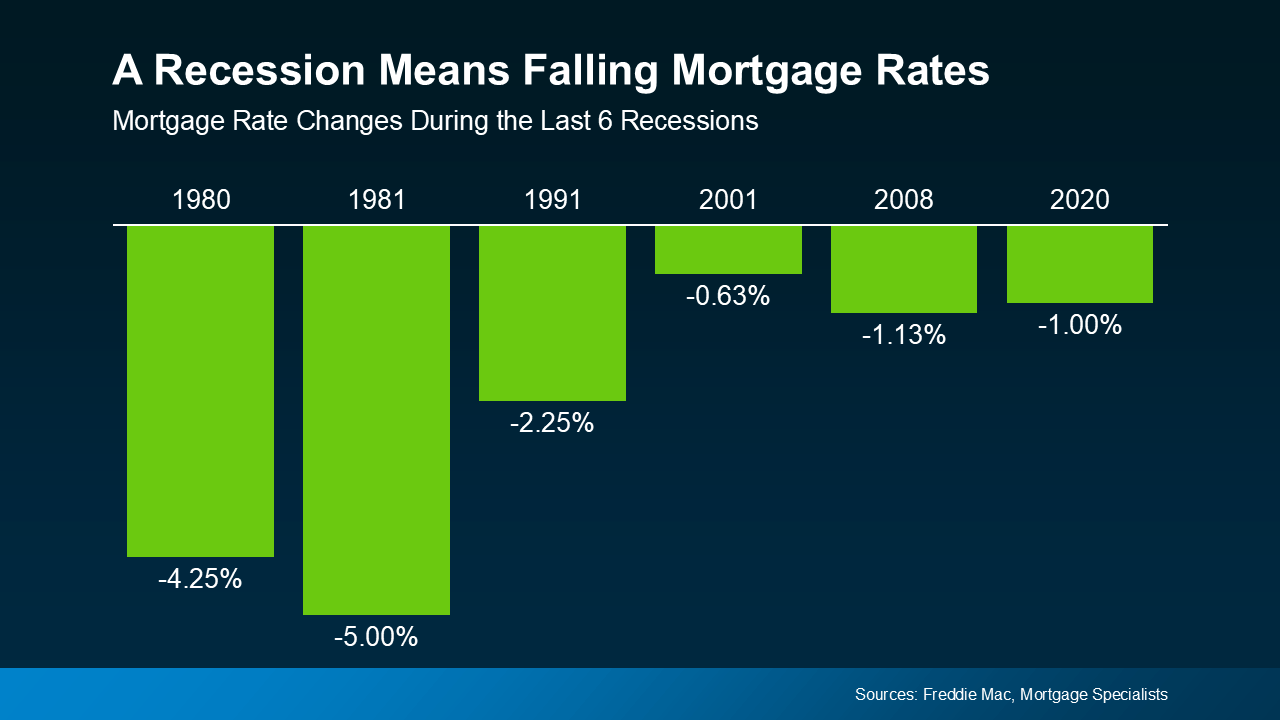

Mortgage Rates Typically Decline During Recessions

While home prices tend to stay on their current path, mortgage rates usually drop during economic slowdowns. Again, looking at data from the last six recessions, mortgage rates fell each time (see graph below):

So, a recession means mortgage rates could decline based on the data. While that would help with affordability, don’t expect the return of a 3% rate.

Bottom Line

The answer to the recession question is still unknown, but the odds have gone up. But that doesn’t mean you have to wonder about the impact on the housing market – historical data tells us what usually happens.

When you hear talk about a possible recession, what concerns or questions come to mind about buying or selling a home?

Richard Iarossi, REALTOR

Coldwell Banker Realty

1300 Main Chapel Way, Gambrills, MD 21054

443.995.9595 Cell

410.721.0103 Office

rich@richsellshomes.com

richsellshomes.com

Townhomes: A Smart Solution for Today’s First-Time Buyers

Buying your first home in today’s market can feel tough. Between high home prices and mortgage rates, affordability is still a big challenge. And some buyers are making one simple trade-off that’s getting them in the door faster: square footage.

According to the National Association of Home Builders (NAHB), 35% of buyers are willing to purchase something smaller to make homeownership happen. And one place you can usually find a smaller footprint (and sometimes better affordability) is in townhomes.

Why Townhomes Are Gaining Popularity

Townhomes typically cost less than single-family homes due to their more limited size. And that’s a big plus for today’s budget-conscious buyer. As Realtor.com says:

“In today’s market, affordability remains a key priority for homebuyers, making townhomes an attractive option because they are often priced more reasonably than single-family homes. It makes them especially appealing to first-time homebuyers on a tighter budget . . .”

So, if you’re trying to buy but feeling stuck because of rising prices, shifting your focus to townhomes could be one way to get into homeownership without maxing out your budget.

Builders Are Responding to the Demand

Builders have seen buyers’ appetite shift to smaller homes, and they’re adjusting to meet the demand. As Joel Berner, Senior Economist at Realtor.com, explains:

“Builders are making a concerted effort to provide smaller, more affordable inventory to the market in a way that the existing-home market cannot. Townhomes are a significant portion of that effort.”

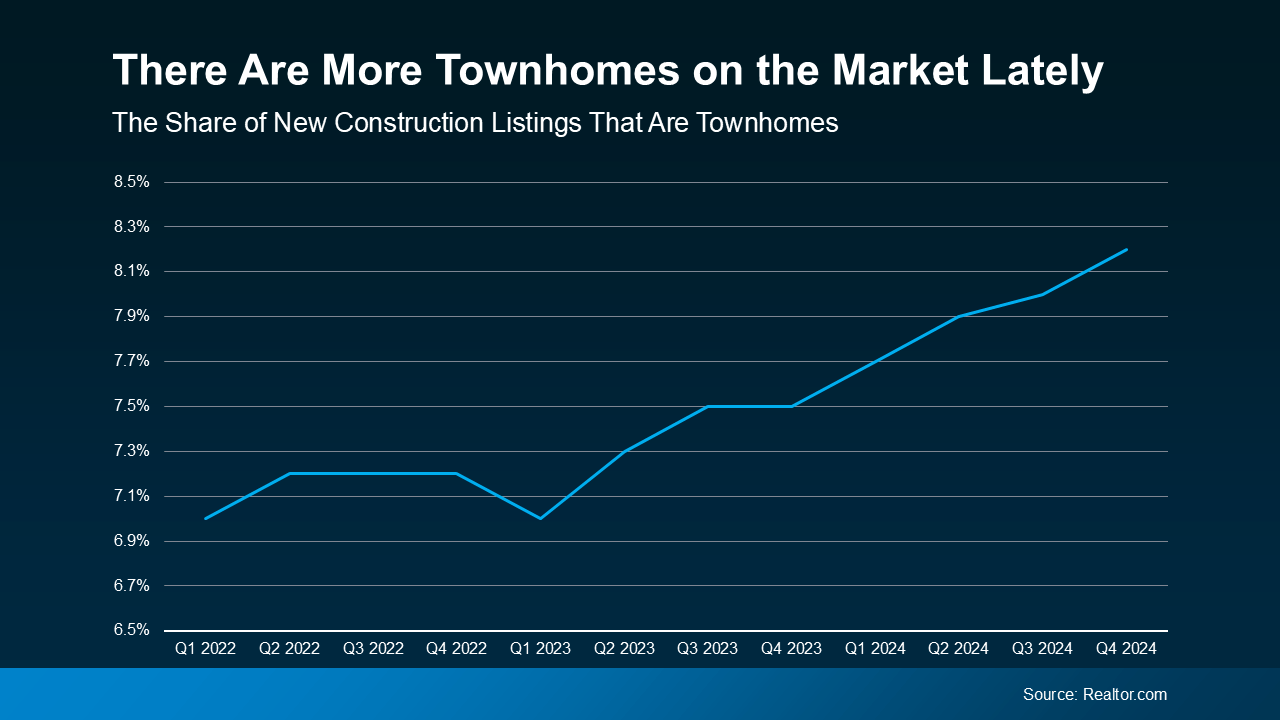

And the numbers back it up. According to data from Realtor.com, townhomes now make up a bigger share of new construction listings than they did just a couple of years ago (see graph below):

That means, if you’re interested in this type of house, you have more choices than you would have had over the last few years. And more options that are potentially more affordable are definitely a good thing. It should make your search for your first home a bit easier.

Is a Townhome Right for You?

If you’ve been focused only on more traditional homes with their own yards, an agent can help you explore whether a townhome could work for you. Who knows, you may find out you love the lifestyle. A lot of people do. As an article from the National Association of Realtors (NAR) explains:

“Townhomes tend to cost less than single-family detached homes and can be appealing to young professionals who may desire medium-density, walkable neighborhoods.”

That’s because they’re lower maintenance, they can provide a sense of community with other residents, and they have their own unique amenities. Not to mention, they give you the chance to start building wealth through homeownership without the upkeep that comes with having your own detached, single-family home. And that can be great for first-time buyers who are a bit worried about the maintenance anyway.

But they also come with some other considerations, like dealing with noise through shared walls. If you’re a renter right now, maybe you’re used to that already. But these are the types of things you’ll want to think about. And that’s where an agent’s expertise comes in. They’ll help you weigh the pros and cons, so you understand how a townhome fits into your lifestyle and long-term goals before making your decision.

Bottom Line

If you’re struggling to find a home within your budget, it may be time to expand your search and consider options you haven’t before, like townhomes. Sometimes, compromising a little bit on space is worth it to get your foot in the door.

What matters most to you — space, location, or budget? Let’s figure out where you can flex to make homeownership happen.

Richard Iarossi, REALTOR

Coldwell Banker Realty

1300 Main Chapel Way, Gambrills, MD 21054

443.995.9595 Cell

410.721.0103 Office

rich@richsellshomes.com

richsellshomes.com

The #1 Thing Sellers Need To Know About Their Asking Price

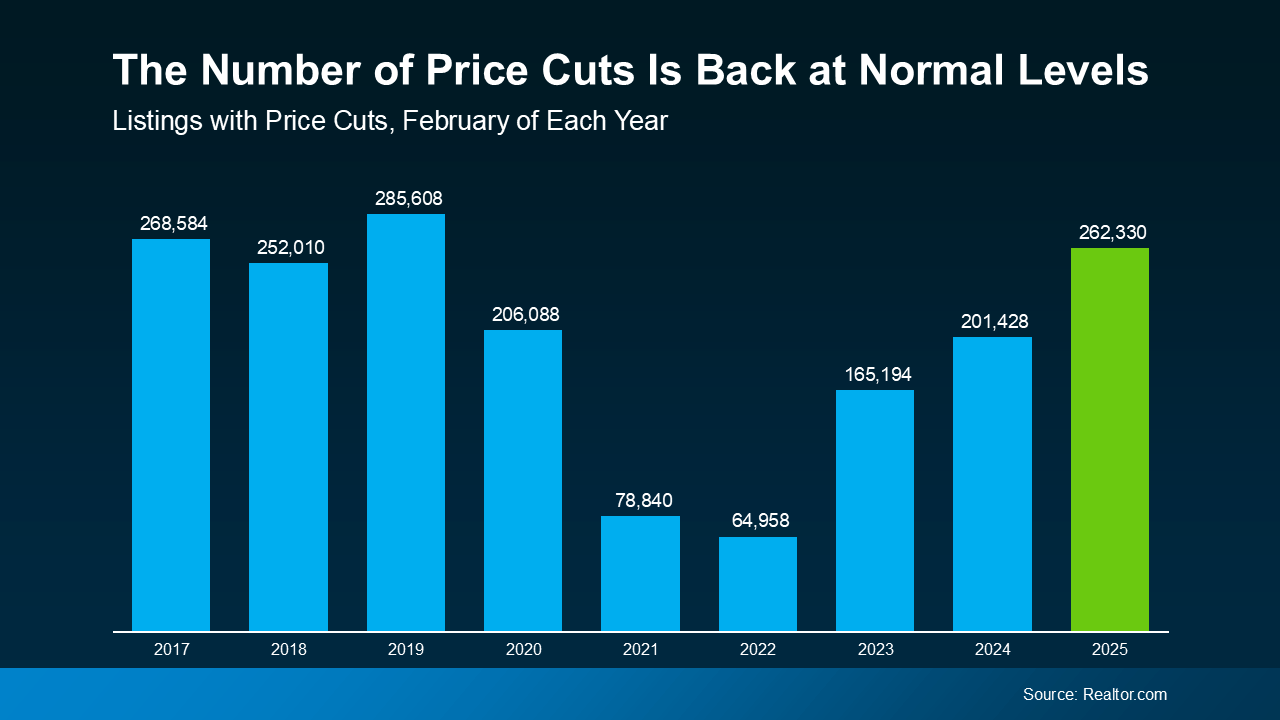

When you put your house on the market, you want to sell it quickly and for the best price possible; that’s generally the goal. But too many sellers are shooting too high right now. They don’t realize the market has shifted as inventory has grown. The side effect? Price cuts are on the rise, but they really don’t have to be. Here’s why.

According to data from Realtor.com, in February, price cuts were the highest they’ve been in any other February since 2019 (see graph below):

If you consider that 2019 was the last true normal year for the housing market – that’s a big deal. We’re getting back to what’s typical for the market.

This isn’t the same frenzied seller’s market we saw a few years ago. You may not get the same price your neighbor did at the height of the pandemic. And that means you may need to reset your expectations.

Because here’s the reality. If you shoot too high and have to lower your price after the fact, you could actually end up walking away with lower offers than if you’d priced it right from the start. So, how do you avoid that? You lean on your agent.

How an Agent Helps You Nail the Right Price

A great agent doesn’t just pull a number out of thin air. They’ll use real data and market trends to make sure your house is priced based on what your specific home is valued at today. So, you’re setting a realistic price – one that’ll draw in serious buyers.

And based on your agent’s analysis of your local market, they may even recommend strategically pricing slightly below market value to help your house attract more eyes and more competitive offers. Here’s how your agent will determine the right number for your house:

They look at recent sales. What did similar homes in your area actually sell for? Not list for, sell for.

They analyze local market trends. Your home’s value isn’t just about what you want for it, it’s about what buyers in your area are willing to pay.

They craft the right strategy. They’ll make sure your home is priced to attract attention and create a sense of urgency among buyers.

Why Overpricing Backfires

Unfortunately, some sellers still ignore their agent’s advice and prefer to start high just to see what happens. The hope being maybe they get their full asking price, or they at least have more wiggle room for negotiation. But pricing high usually ends up costing you, and here’s why:

Buyers may not even look at it. Today’s buyers are more budget-conscious than ever. If they see a home that seems overpriced, they’re likely to skip it completely rather than try to negotiate.

It could sit on the market for too long. The longer your home sits unsold, the more buyers will assume something’s wrong with it. That can make it even harder to sell down the line.

You might end up getting less. Homes that require a price cut often sell for less than they would have if they had been priced right from the start.

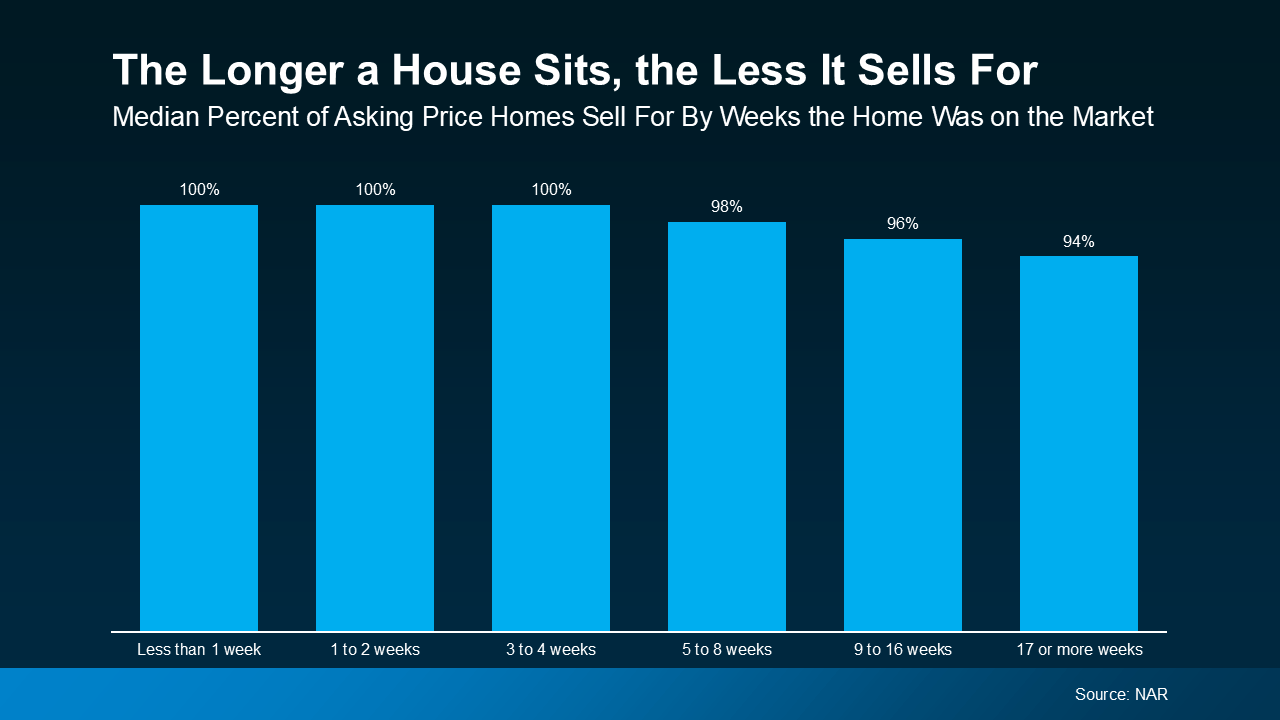

You can see that shake out in the graph below. It uses data from the National Association of Realtors (NAR) to show that the longer a house sits, the less it’ll sell for:

This graph shows that if a house sells within the first 4 weeks it is listed, it usually goes for full price. Based on experience, that’s what usually happens to homes that are priced at or just below current market value. If it’s priced right, buyers will be interested, and, ultimately, willing to pay the asking price – or compete with other buyers and even go over asking.

But if a house isn’t priced right, it doesn’t sell as quickly. And this graph shows that, after the first 4 weeks on the market, the price starts to drop from there. That’s because buyer interest falls off the longer it sits. So, it becomes more likely a seller will either accept a lower offer because that’s all they have, or opt to do a price drop to draw people back in.

Bottom Line

The last thing you want is to list too high, watch your house sit, and then have to drop the price just to get attention. Let’s connect so that doesn’t happen to you.

Want to make sure your home sells quickly and for the best price? Let’s go over the right pricing strategy for your house.

Richard Iarossi, REALTOR

Coldwell Banker Realty

1300 Main Chapel Way, Gambrills, MD 21054

443.995.9595 Cell

410.721.0103 Office

rich@richsellshomes.com

richsellshomes.com

Buyers Have More Negotiation Power – Here’s How To Use It

You may have heard there are more homes for sale right now. And while that’ll vary depending on the market, it means that overall, things are starting to lean in a more balanced direction. As that happens, some sellers are a bit more open to compromise. Here’s what that means for you.

You may be regaining some negotiating power. That can translate into savings, perks, or even better terms on your purchase – if you know what levers to pull during negotiation.

Why an Agent Is an Essential Part of the Negotiation Process

The complicated part is knowing what is and isn’t on the table. That’s where your agent comes in. According to the National Association of Realtors (NAR), besides finding the right home, the top thing buyers want from their agent is help negotiating the terms of the sale, followed by negotiating the price.

Here’s why. Agents are skilled negotiators and are trained for moments like this. Since your agent is an expert on the local market, they’ll also know what’s working for other buyers (and what’s not), and that can help you get a better understanding of what’s realistic to ask for.

What’s on the Negotiation Table?

Here are some of the most common concessions an agent can help you negotiate:

Sale Price: The most obvious concession is the price of the home. And that lever is being pulled more often today. Buyers don’t want to overpay when affordability is already so tight. And sellers who aren’t realistic about their asking price may have to consider adjusting their price.

Closing Costs: Closing costs are usually about 2-5% of a home’s purchase price and include fees for things like the appraisal, title insurance, and underwriting of your loan. To offset the cash you have to bring to the table, you can ask the seller to pay for some or all of these expenses. This was the most common concession sellers made in 2024, according to NAR.

Home Warranties: If you’re worried about the maintenance costs that may pop up after you get the keys, you can ask the seller to pay for a home warranty. Since this concession usually isn’t terribly expensive for the seller, it can be a good negotiation tool for a buyer. It’s not a big cost for them, but it can be a big perk for you.

Home Repairs: Based on the inspection, you’re within your rights to ask the seller to make repairs. If the seller doesn’t want to, they could offer to drop the home price or cover some closing costs, so you have more room in your budget to take care of the repairs yourself.

Fixtures: Want that washer and dryer to stay? Maybe the stainless-steel fridge, too? In many cases, you can ask for appliances or even furniture to be included in the deal, which will save you money when you move in.

Closing Date: The closing date is also negotiable. Based on your timeline, you may also request a faster or extended closing window. Depending on the seller’s needs, this could be great for their situation, too.

Of course, negotiating is a complex process. And not every seller will be willing to offer concessions. Again, lean on your agent for expert advice about what’s realistic to ask for and what could turn sellers off.

Because once you’ve found a home you love, you don’t want to risk losing it. But you also want to get the best terms possible on your purchase – and that’s where an agent can make all the difference.

Bottom Line

As inventory grows, buyers are finding they have a bit more leverage. And having the right agent by your side – who can help you approach negotiations strategically – is key.

What’s your biggest concern when it comes to negotiating with a seller? Let me know and we’ll put together a solid plan that makes things less stressful.

Richard Iarossi, REALTOR®

Coldwell Banker Realty

1300 Main Chapel Way, Gambrills, MD 21054

443.995.9595 C

410.721.0103 O

rich@richsellshomes.com richsellshomes.com

Spring is in full swing, and the housing market is picking up along with it. And if you’ve been wondering whether now is the right time to buy or sell, here’s the inside scoop on why this spring may be a great time to make your move.

1. There Are More Homes for Sale

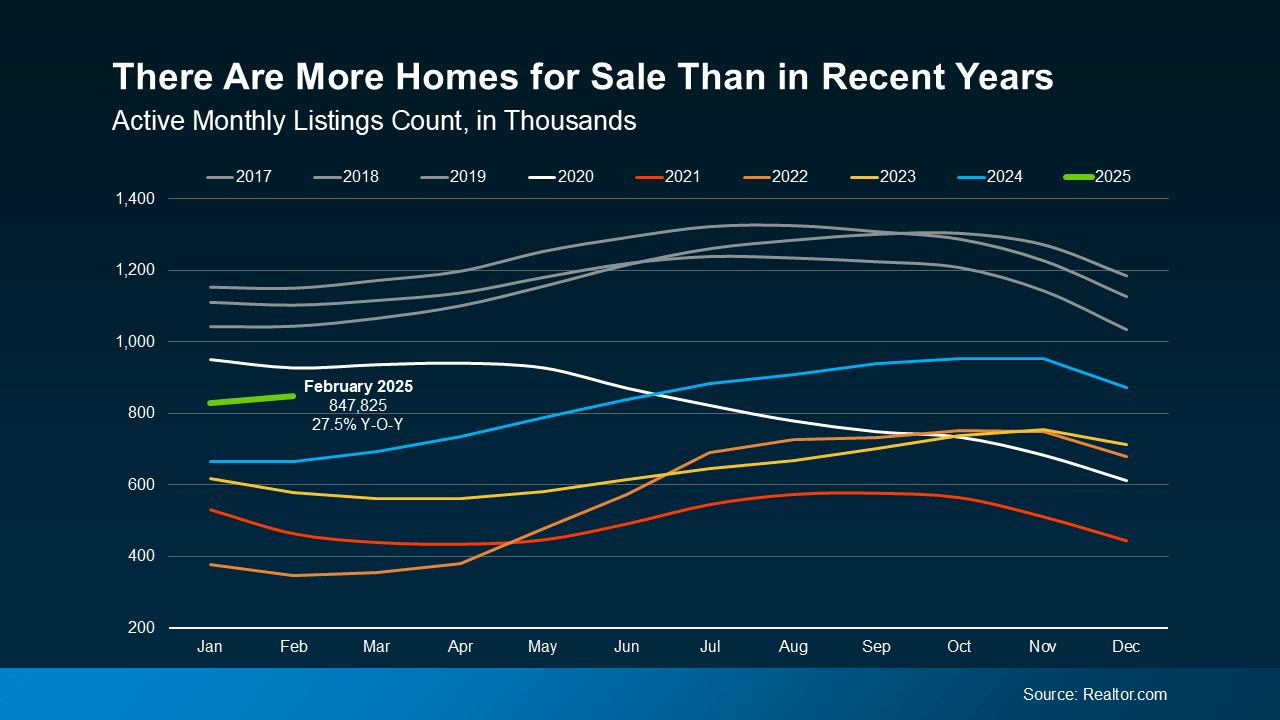

After a long stretch of tight inventory, the number of homes for sale is finally improving. According to recent national data from Realtor.com, active listings are up 27.5% compared to this time last year.

Look at the graph below and follow the green line for 2025. You can see, even though inventory levels still haven’t returned to pre-pandemic norms (shown in gray), that number is higher than it has been going into the spring market over the past few years (see graph below):

Buyers: This means you have more choices, and you can be more selective.

Sellers: With more homes available than in recent years, you’re more likely to find what you’re looking for when you move. And knowing that inventory is still below more normal levels means there will be demand for your home when you sell it, too.

2. Home Price Growth Is Moderating

As inventory grows, the pace of home price growth is slowing down – and that will continue into the spring market. This is because prices are driven by supply and demand. When there are more homes for sale, buyers have more options, so there’s less competition for each house. Rising supply and less buyer competition causes price growth to slow, but it should still remain positive in most markets. As Freddie Macsays:

“In 2025, we expect the pace of house price appreciation to moderate from the levels seen in 2024, while still maintaining a positive trajectory.”

And while prices aren’t dropping at the national level, every market is different. Some areas are seeing stronger price growth, while others are cooling off or even seeing some price declines.

Buyers: The slower pace of growth means prices aren’t rising as quickly as before – and that’s a relief. Any home you buy now is likely to appreciate in value over time, helping you build equity.

Sellers: While prices are still rising, you might need to adjust your expectations. Overpricing your house in a more balanced market could mean it takes longer to sell. Pricing your house competitively is going to be key to attracting offers.

3. Mortgage Rates Are Stabilizing

One of the biggest hurdles for buyers over the past couple of years has been high, volatile mortgage rates. But there’s some good news – overall, they’ve stabilized in recent weeks – and have even declined a bit since the beginning of this year. And while that decrease hasn’t been a big drop, stabilizing mortgage rates has helped make buying a home a bit more predictable. According to Selma Hepp, Chief Economist at CoreLogic:

“With the spring homebuying season upon us, the recent improvements in mortgage rates may help invite homebuyers back into the market.”

Buyers: When mortgage rates are more stable, it’s easier to plan ahead because you have a better idea of what your future payment might be. But remember, rates will continue to be volatile. So, lean on your agent and your lender to make sure you know what the latest mortgage rate means for you.

Sellers: Slightly lower rates that are starting to stabilize are encouraging more buyers to move forward with their plans. That’s good for demand when you’re planning to sell your house.

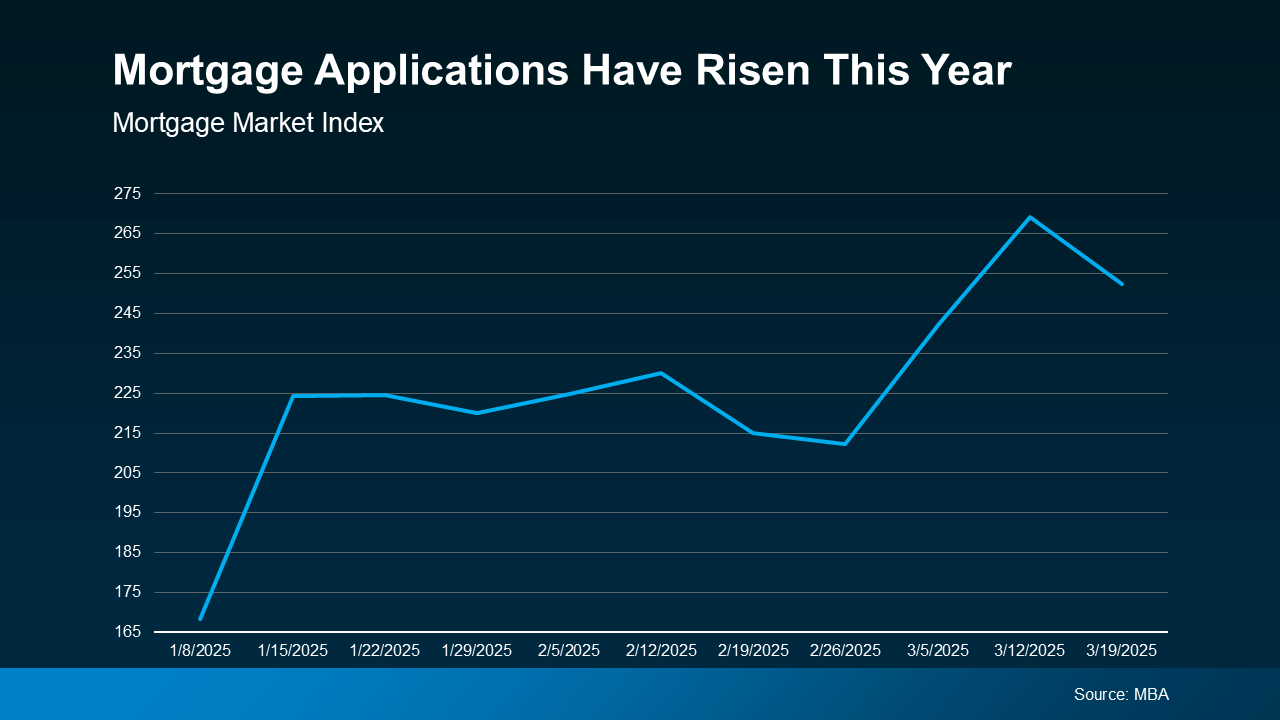

4. More Buyers Are Returning

With more inventory, slowing price growth, and stabilizing mortgage rates, buyers are gaining confidence and coming back into the market. Demand is picking up, and data from the Mortgage Bankers Association (MBA) shows an increase in mortgage applications compared to the start of the year (see graph below):

Buyers: Acting sooner rather than later could be a smart move before your competition heats up even more.

Sellers: This is great news for you – more buyers mean a better chance of selling your house quickly.

Bottom Line

Do you have questions about what the spring market means for you? Let’s connect and talk about how to craft your plan this season.

With more homes for sale, slowing price growth, and stabilizing mortgage rates, how will this impact your decision to buy or sell this spring?

Richard Iarossi, REALTOR®

Coldwell Banker Realty

1300 Main Chapel Way, Gambrills, MD 21054

443.995.9595 C

410.721.0103 O

rich@richsellshomes.com

richsellshomes.com

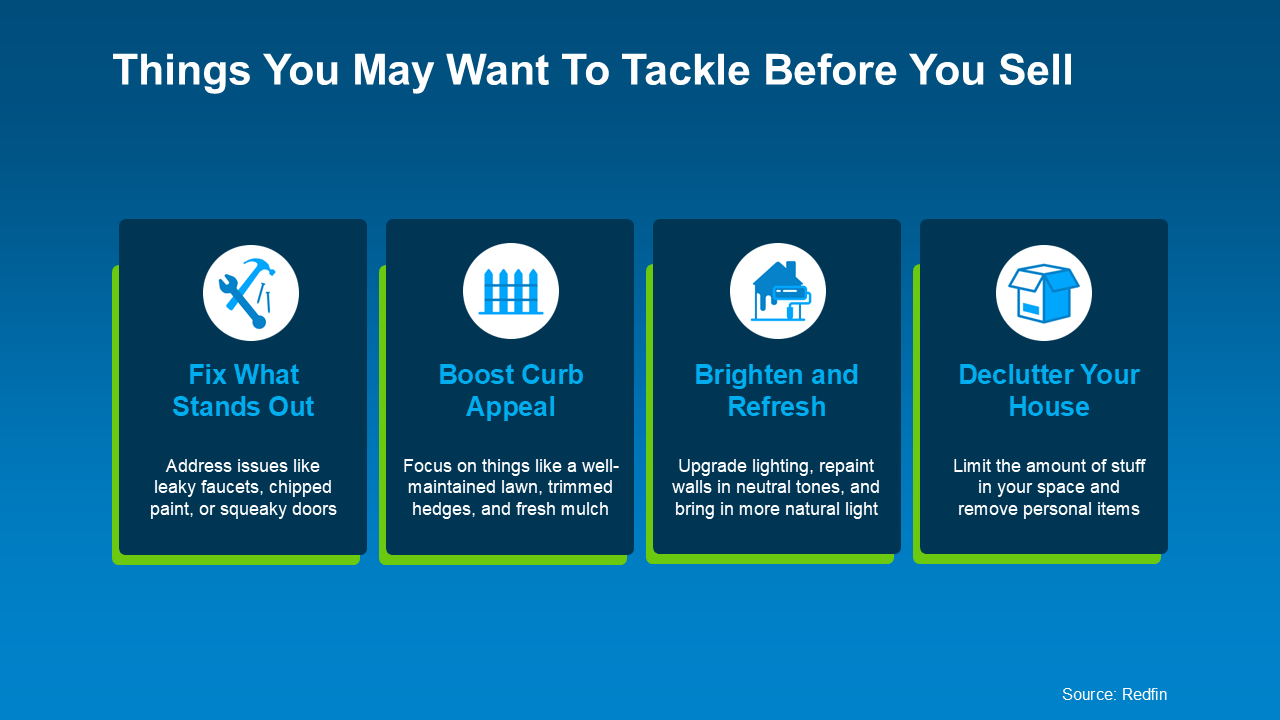

The Best Week To List Your House Is Almost Here – Are You Ready?

If selling your house is on your to-do list this year, the time to start prepping is now. That’s because experts say the best week to list your house is coming up fast.

A recent Realtor.comstudy analyzed years of housing market trends (excluding 2020 since it was an outlier) and found that April 13–19 is expected to be the ideal window to put your house on the market this year:

“. . . we’ve identified April 13-19 as the best week to list for sellers . . . a seller listing a well-priced, move-in ready home is likely to find success. Because spring is generally the high season for real estate activity and buyers are more plentiful earlier rather than later in the year, listing earlier in the spring raises a seller’s odds of a successful sale.”

What Makes This Week Stand Out?

As the quote mentions, spring is almost always a strong season for sellers. But this particular week could give you an even bigger advantage this year. Realtor.com goes on to say what listing during this sweet spot could mean for you:

More buyers looking at your home since demand is high this time of year.

A faster sale since serious buyers are eager to move before summer.

A better chance of selling for top dollar. According to the study, you could get an average of $4,800 more this week (and $27,000 more than you would earlier in the year).

If You Want Your House on the Market for that Window, Act Now

With just a few weeks left before this prime listing window, you’ll need to make a plan to work smart and act fast. That’s where working with a great real estate agent comes in. They can help you:

Figure out exactly what you need to do to get your house ready.

Prioritize the tasks that’ll make the biggest impact in the shortest time.

Decide if there are any quick fixes or small upgrades that could help you attract buyers.

Assuming your house is already in good shape, your focus should be on quick, high-impact updates. As Investopedia explains:

“You won’t have time for any major renovations, so focus on quick repairs to address things that could deter potential buyers.”

Here are a few examples of small projects that can make a big difference according to Redfin:

What If You’re Not Ready Just Yet?

Don’t worry – it’s okay if you don’t think you’ll be ready for this week. Just because April 13–19 is projected to be the ideal week by Realtor.com, that doesn’t mean it’s the only good time to sell. Even if you need a bit more time to get your home list ready, there’s still plenty of opportunity this homebuying season.

Bottom Line

If you’ve been waiting for the right time to sell, this could be it. But timing isn’t the only thing that matters – how well you prep and price your home is just as important.

What’s one thing you’d need to do before you’d feel ready to list? Let’s connect and figure out the best plan to make it happen.

Richard Iarossi, REALTOR®

Coldwell Banker Realty

1300 Main Chapel Way, Gambrills, MD 21054

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Buyers: This means you have more choices, and you can be more selective.

Buyers: This means you have more choices, and you can be more selective. Buyers: Acting sooner rather than later could be a smart move before your competition heats up even more.

Buyers: Acting sooner rather than later could be a smart move before your competition heats up even more.