Why Pre-Approval Is More Important Than Ever This Spring

Spring is here, and so is the busiest season in real estate. More buyers are out looking for homes, which means more competition for you. If you want to put yourself in the best position to buy, there’s one step you can’t afford to skip, and that’s getting pre-approved for a mortgage.

Some buyers think they can wait until they’ve found a home they love before talking to a lender. But in a season where homes can sell fast, that’s a risky move. Getting pre-approved before you start your search is a much better bet.

Here’s what you need to know about this early step in the buying process.

What Is Pre-Approval?

Pre-approval gives you a sense of how much a lender is willing to let you borrow for your home loan. To determine that number, a lender starts by looking at your financial history. Here are some of the things that can have an impact, according to Yahoo Finance:

Your debt-to-income (DTI) ratio: This is how much money you owe divided by how much money you make. Usually, you can borrow more if you have a lower DTI.

Your income and employment status: They’re looking to verify you have a steady income coming in – that way they feel confident in your ability to repay the loan.

Your credit score: If your score is higher, you may qualify to borrow more.

Your payment history: Do you consistently pay your bills on time? Lenders want to know you’re not a risky borrower.

After their review, you’ll get a pre-approval letter showing what you can borrow. Having this peace of mind is a big deal – it helps you feel a lot more confident in your ability to get a home loan. And the fringe benefit is it can also speed up the road to closing day because the lender will already have a lot of your information.

It Helps You Figure Out Your Budget

Spring is a competitive season, and emotions can run high if you find yourself up against other buyers. Having a firm budget in mind is so important. You don’t want to get too attached and end up maxing out what you can borrow. As Freddie Mac explains:

“Keep in mind that the loan amount in the pre-approval letter is the lender’s maximum offer. Ultimately, you should only borrow an amount you are comfortable repaying.”

So, use this time to really buckle down on your numbers. And be sure to factor in other homeownership costs – like property taxes, insurance, and maybe even homeowner’s association fees – so you know what you can comfortably afford.

Then, partner with your agent to tailor your search to homes that match your budget. That way, you don’t fall in love with a house that’s out of your financial comfort zone.

It Helps Your Offer Stand Out During the Busy Season

Spring buyers aren’t just competing for homes. They’re competing for the seller’s attention, too. And a pre-approval letter can help you stand out by showing sellers you’ve already gone through a financial check. Zillow explains it like this:

“Having a pre-approval letter handy while you’re shopping for a home can also help you act quickly once you’ve found a home you love. The letter shows potential sellers that you’re a serious buyer who has the financial means to close on the home. In a competitive market, an offer with a pre-approval letter attached will stand out among other offers that don’t include one — increasing the chances of your offer being accepted.”

That means when sellers are choosing among multiple offers, yours could rise to the top simply because you’ve already taken this step.

And here’s one final tip for you. After you receive your letter, avoid switching jobs, applying for new credit cards or other loans, co-signing for loans, or moving money in or out of your savings. That’s because any changes to your finances can affect your pre-approval status.

Bottom Line

If you’re thinking about buying a home this spring, getting pre-approved should be your first move. It’ll help you understand your budget, show sellers you’re serious, and keep you from falling in love with a house that’s out of reach. Talk to a lender to get started.

What’s your plan to stand out in this competitive market? Let’s chat about how to make sure you’re fully ready to buy.

Richard Iarossi, REALTOR®

Coldwell Banker Realty

1300 Main Chapel Way, Gambrills, MD 21054

443-995-9595 C

410-721-0103 O

rich@richsellshomes.com

richsellshomes.com

Breaking Into the Market: Smart Moves for First-Time Buyers

If you’re like a lot of aspiring homebuyers, there’s a major hurdle standing in your way — the cost of living. From groceries to gas, eggs, and just about everything else, prices have gone up. And that rings true for home prices, too.

But even when everything feels expensive, there are still ways to make homeownership more than an item on your wish list. You may just need to think about where you plan to buy a bit differently.

Think of Your First Home as a Stepping Stone

One of the biggest misconceptions among buyers is that their first home has to be their forever home – or that it has to check all the boxes of what they want right out of the gate. In reality, it’s just a starting point.

Once you own a home, you start to build equity, which grows over time as home prices rise. Down the road, if you want to move — whether to a larger space, a better location, or both — the equity you’ve gained can help you do just that.

So rather than waiting until you can afford your dream home in your ideal neighborhood, consider starting with something that works for now.

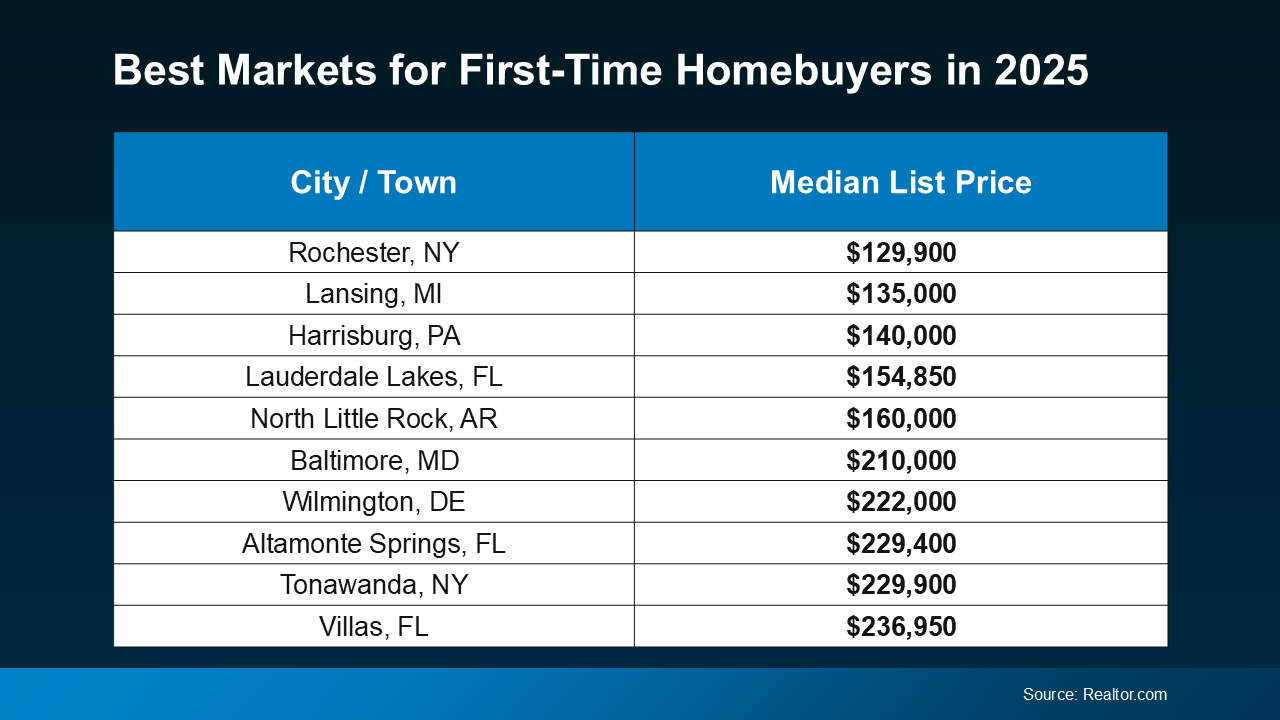

Expand Your Search To Find More Affordable Options

If high home prices in your favorite area are holding you back, it’s time to cast a wider net. By keeping an open mind and being flexible with location, you may be surprised at what’s possible within your budget. Many buyers find success by looking in surrounding areas – and some even choose to move out of state.

According to a report from Realtor.com, these are some of the best markets for first-time homebuyers this year (see chart below):

Of course, moving to a different state isn’t for everyone – and isn’t a necessity. The right agent can help you find more cost-effective options wherever you are.

If you want to stay local, looking just outside your preferred neighborhood could help you find something you can afford that’s still pretty close to your favorite restaurants, shops, and activities. Sometimes, moving as little as 10 minutes away makes a big difference.

And the best way to see what’s available is to work with a real estate agent who understands the local market and can help you identify hidden gems nearby. An agent can point you to communities you may not have considered that have lower price tags now and are steadily gaining value and appeal. That way you can buy your first home and be set up to gain equity through the years.

Bottom Line

Today’s cost of living is a challenge for many homebuyers. But by exploring different areas and working with a knowledgeable agent, you can take that first step toward owning a home — and building equity for your future.

How far outside of your area would you look to make homeownership happen? Let’s connect to chat through your options.

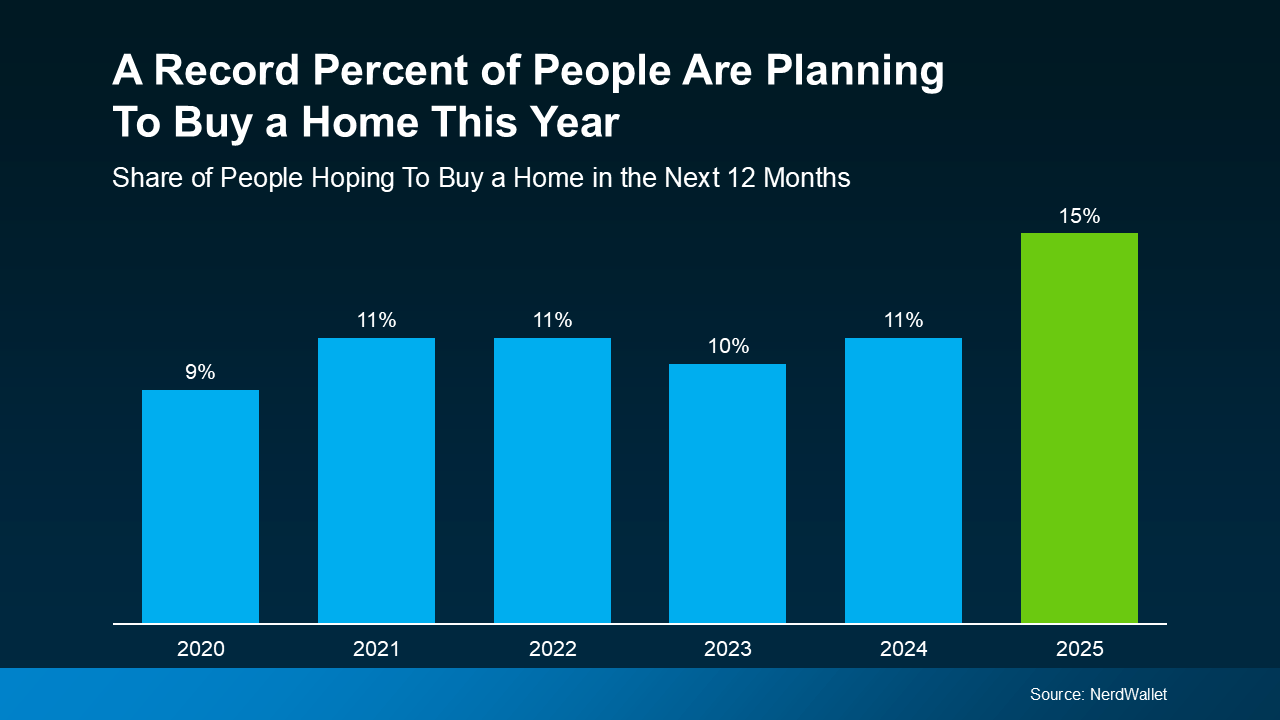

A Record Percent of Buyers Are Planning To Move in 2025 – Are You?

This could be the year to sell your house – and here’s why. According to a recent NerdWallet survey, 15% of people are planning to buy a home this year. That’s actually a record high for this survey (see graph below):

Here’s why this is such a big deal. The percentage has been hovering between 9-11% since 2020. This recent increase shows buyer demand hasn’t disappeared – if anything, it indicates there’s pent-up demand ready to come back to the market.

That doesn’t mean the floodgates are opening and that there’s going to be a huge wave of buyers like we saw a few years ago. But this does signal there’ll be more activity this year than last.

At least some of the buyers who put their plans on hold over the past few years will jump back in. Whether they’re feeling more confident about moving, they’ve finally saved up enough to buy, or they simply can’t wait any longer – this is the year they’re aiming to take the plunge.

And, according to that same NerdWallet survey, more than half (54%) of those potential buyers have already started looking at homes online.

That’s a good indicator that a number of these buyers will be looking during the peak homebuying season this spring. So, if you find the right agent to make sure your house is prepped, priced, and marketed well, you can get your house in front of them.

Bottom Line

More people are going to move this year, and with the right strategy, you can make sure your house is one of the first they look at.

What do you think these buyers will love most about your house?

Let’s talk it over and make sure it’s front and center in your listing.

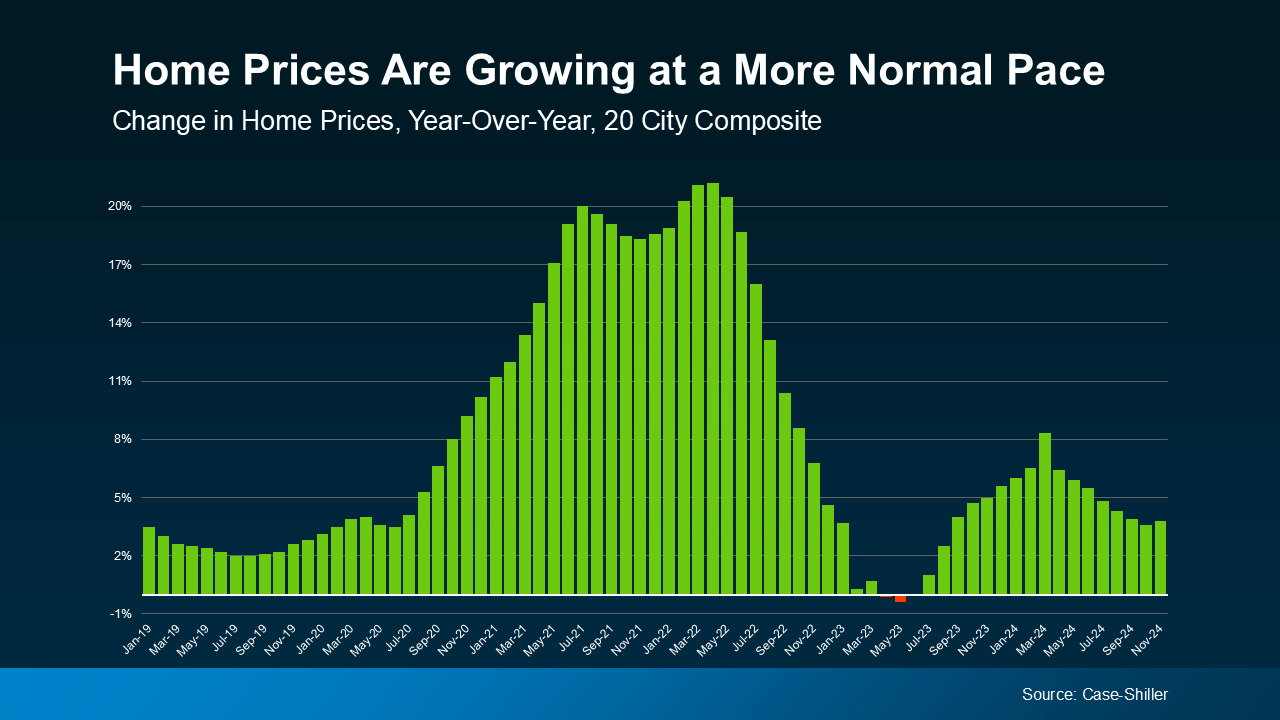

Home Price Growth Is Moderating – Here’s Why That’s Good for You

Over the past few years, home prices skyrocketed. That’s been frustrating for buyers, leaving many wondering if they’d ever get a shot at owning a home. But here’s some welcome news: that whirlwind pace of home price growth is slowing down.

Home Prices Are Rising at a Healthy Pace

At the national level, home prices are still going up, but at a much more moderate, normal pace. For example, in November, the year-over-year increase in home prices was just 3.8% nationally, according to Case-Shiller. That’s a far cry from the double-digit spikes that occurred in 2021 and 2022 (see graph below):

This more normal home price growth might make buying a home feel more attainable for many buyers. You won’t face the same sticker shock or rapid price jumps that made it hard to plan your purchase just a few years ago.

At the same time, steady growth means the home you buy today will likely appreciate in value over time.

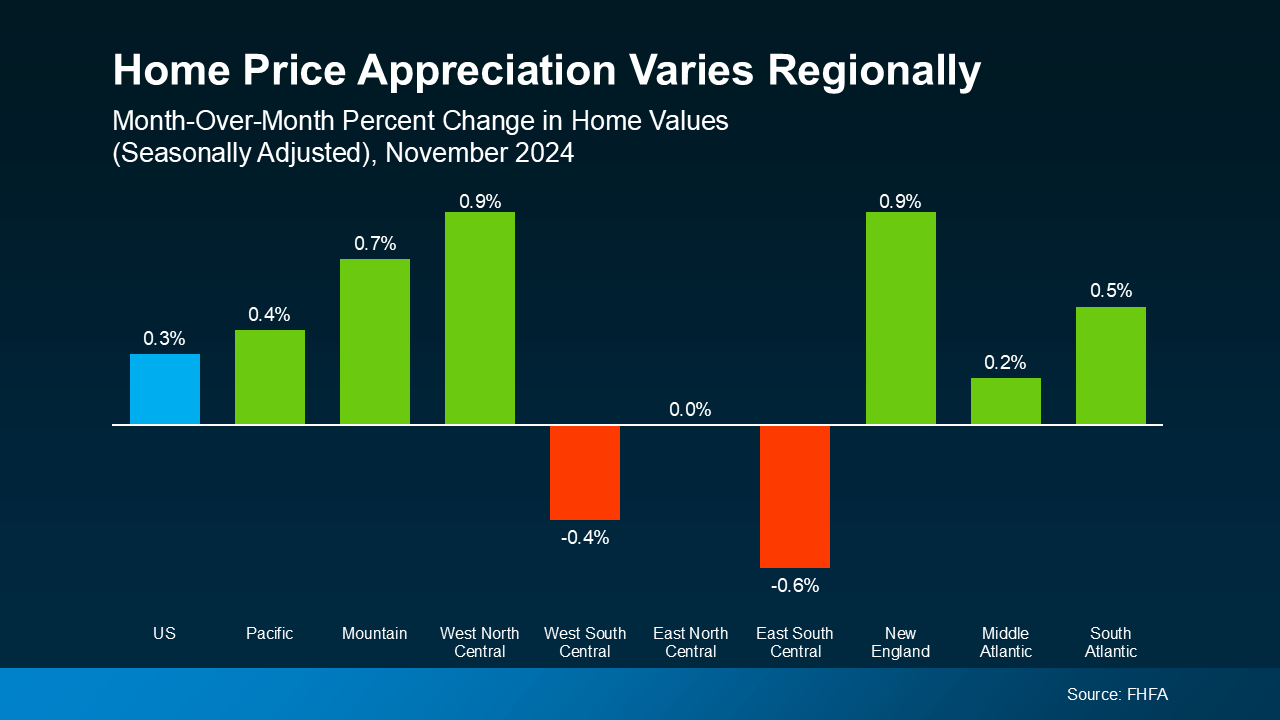

Prices Vary from Market to Market

While the national story is one of moderate price growth, it’s important to remember that all real estate is local. Some markets are seeing stronger growth, while others are cooling off or even seeing slight declines. As Selma Hepp, Chief Economist at CoreLogic, notes:

“Regionally, variations persist, as some affordable areas – including smaller metros in the Midwest — remain in high demand and continue to see upward home price pressures.”

Meanwhile, other regions saw slight month-over-month declines in November, according to Federal Housing Finance Agency (FHFA) data (see graph below):

What does this mean for you? It’s crucial to understand what’s happening in your local market. A national average can’t tell the whole story. That’s where working with a local real estate agent can really help. They have the tools and expertise to give you the full picture of what’s happening in your area and how to plan for that in your move.

Bottom Line

Home prices are growing at a more manageable pace, and working with a local real estate agent can help you navigate the ups and downs of your specific market.

How have changing home prices impacted your plans to buy? Let’s talk about it.

The Secret To Selling This Spring: Start the Prep Work Now

Spring is the busiest season in the housing market. It’s the time of year when buyers are most active – that means it’s when homes sell faster and for top dollar. If you’ve already got a move on your mind, why not list this spring and take advantage of the added buyer demand?

Since spring is just around the corner, now’s the time to start getting your house market-ready. You’ve got just over a month to do the prep work. And while that may sound like a decent amount of time, it’s going to go by quickly. And you won’t want to rush through this important task – especially this year.

The Right Repairs Will Matter More This Spring

Right now, two things are true. There are more homes on the market than there have been in years. And buyers are being extra selective. That combination means you need to invest some time and effort in making strategic repairs. And many homeowners already have a jump on this work.

In the 2025 Outlook for Home Remodeling, Carlos Martin, Director of the Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University, explains:

“. . . homeowners are slowly but surely expanding the pace and scope of projects compared to the last couple years.”

And the most common projects they’re tackling are replacing water heaters, HVAC units, and flooring. Energy efficiency is a key consideration too, based on home improvement data from the Census.

What To Prioritize as You Plan Ahead

But just because that’s what other homeowners are doing, it doesn’t mean that’s what you have to tackle. Think about what you’d want to see if you were a buyer. Focus on quick wins that are easy to knock out with the time you have – but, don’t ignore key repairs, especially ones you think could turn off buyers.

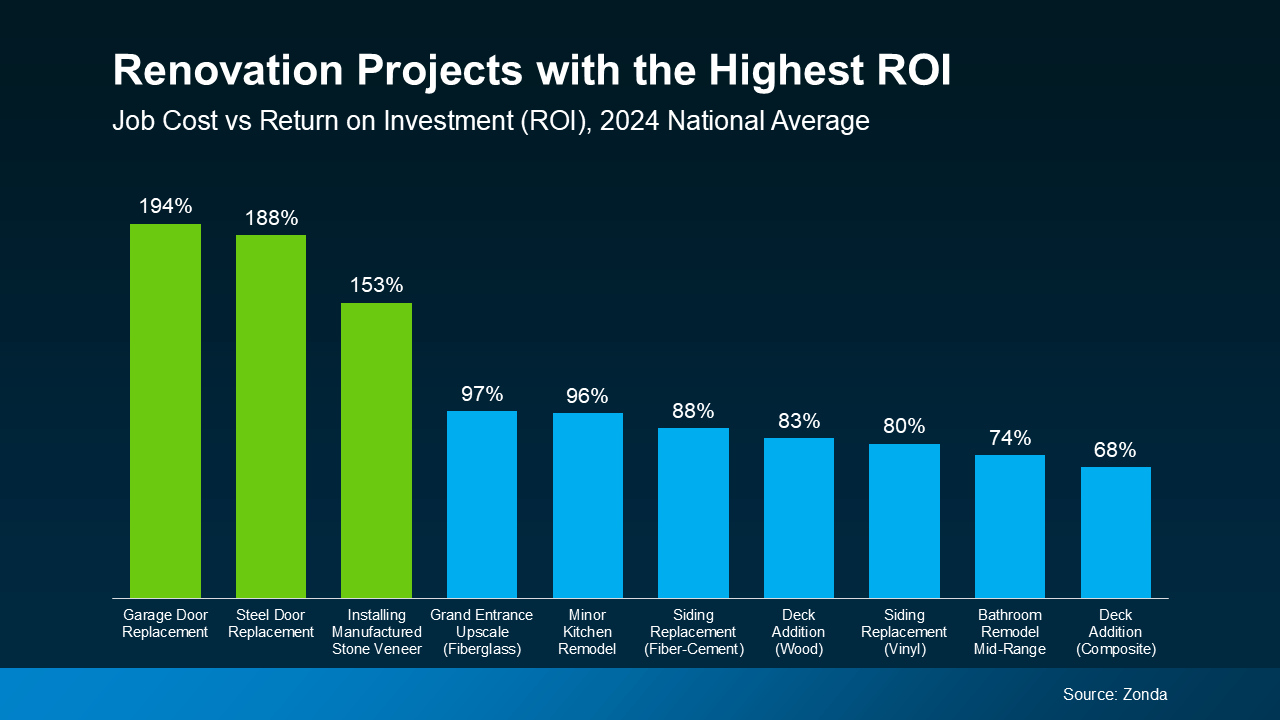

While big-ticket items like replacing an old roof or outdated flooring may seem daunting, they can pay off – especially if you focus on projects with the best return on investment (ROI).

An agent’s expertise is key in narrowing down your list to what’s actually worth it. They know what buyers in your area want and they also have data like this report from Zonda to guide you on which updates have the best ROI(see green in the graph below):

That’s why it’s so important to talk to a local real estate agent before you dive into any repairs. Bankrate puts it best:

“As a seller, it’s smart to be prepared and control whatever factors you’re able to. Things like hiring a great real estate agent and maximizing your home’s online appeal can translate into a smoother sale — and more money in the bank.”

It’s not too early to partner with an agent. By starting now, you’ve still got time to space out the work and find any contractors you need to get the job done. If you wait until spring to roll up your sleeves, you risk running out of time – and that means your house may be overshadowed by others who are more buyer-ready.

Bottom Line

If you’re planning to sell this spring, it’s time to start tackling your to-do list. But, before you get started, let’s connect. That way you can make sure you’re spending your time and budget on projects that’ll pay off in the long run.

Send me a list of what’s on your to-do list, and we can prioritize them together.

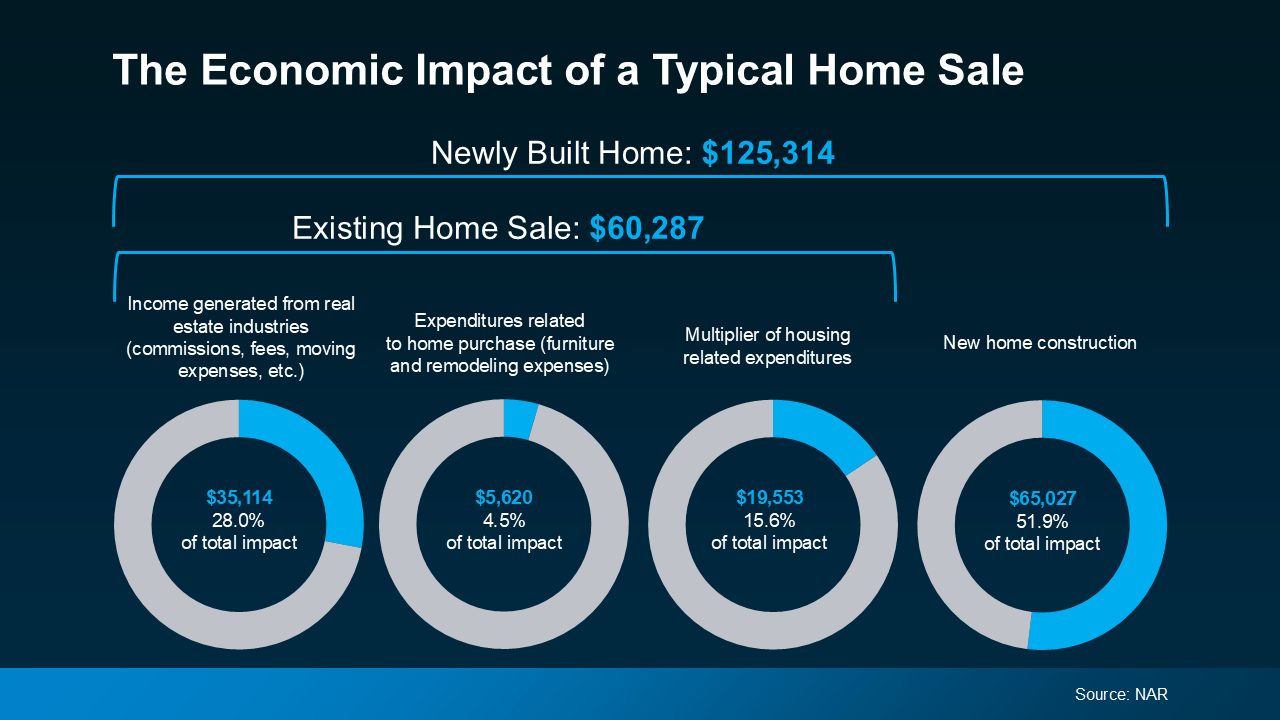

How Buying or Selling a Home Helps Your Local Economy

Whether you’re buying or selling a house, here’s something to think about that most people don’t. Your decision doesn’t just impact your life and your family’s, it sparks a ripple effect that has a positive impact on your entire community.

Every year, the National Association of Realtors (NAR) puts out a report that breaks down the financial impact that comes from people buying and selling homes.

The data shows that if you buy an existing (previously lived-in) home, you’re giving the local economy a boost of just over $60K. And if you buy a newly built home, that number goes up to over $125K (see visual below):

That’s because of all the people needed to build, fix up, and sell homes. Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB), explains how the housing industry adds jobs to a community:

“. . . housing is a significant job creator. In fact, for every single-family home built, enough economic activity is generated to sustain three full-time jobs for a year . . .”

When you think about it, it makes sense. Behind every home sale is a network of people involved, including contractors, city officials, real estate agents, lawyers, specialists, and more. Everyone has a job to do to help make sure your deal goes through.

Put simply, when you buy or sell a home, you’re helping out your neighbors. So, your decision to move doesn’t just meet your needs; it supports their families, strengthens your town, and shapes the future of your community.

Imagine walking through the front door of your next home, knowing your decision helped a local contractor keep their crew working or a small business thrive. Remember that feeling as you make your decision this year.

Bottom Line

Moving isn’t just a personal milestone – it’s an investment in your community, too. If you’re ready to make a move, let’s connect. You’ll make a difference for more people than you know.

What’s most important to you as you prepare to buy or sell your house this year?

Richard Iarossi, REALTOR

Coldwell Banker Realty

1300 Main Chapel Way, Gambrills, MD 21054

443-995-9595 Cell

410-721-0103 Office

richard.iarossi@cbmove.com

richsellshomes.com

Homeowner’s insurance is a must-have to protect what’s probably your biggest investment – your home. And while you never want to think about worst-case scenarios, the right coverage is basically your safety net if something goes wrong. Here’s how it helps you.

Covers Repairs and Rebuilding Costs: If your home is damaged by fire, storms, or other covered events, your policy helps pay for repairs or even a full rebuild.

Protects Your Belongings: Many policies can also cover personal items like furniture, electronics, and clothing if they’re stolen or damaged.

Provides Liability Coverage: If someone gets injured on your property, homeowner’s insurance can help cover medical bills or legal expenses.

In the simplest sense, it gives you peace of mind. Knowing you have protection against unexpected events helps you worry less. And with such a big purchase, having that reassurance is a big deal.

And while your first insurance payment will be wrapped into your closing costs, you’ll want this to be a part of your budget beyond closing day too. That’s because it’s a recurring expense you’ll have once you get the keys to your home.

Here’s what you need to know to help you budget for this important part of homeownership today.

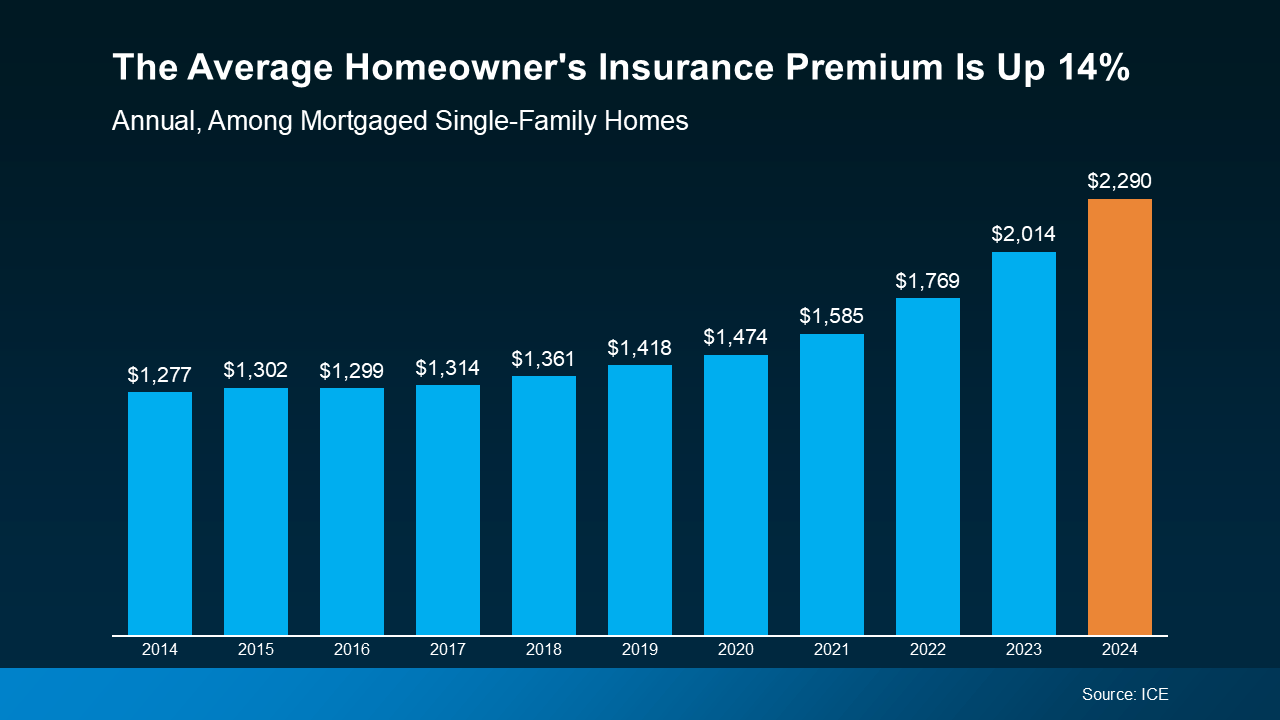

Costs and Claims Are Rising

In recent years, insurance costs have been climbing. According to Insurance.com, there are four big reasons behind the jump in premiums:

More severe weather events and wildfires are leading to higher claims.

Insurance companies are pulling out of high-risk areas, reducing options for homeowners in some states.

Past rate increases haven’t kept up with the rise in claims.

The cost to rebuild or repair homes has gone up due to higher material and labor costs.

Basically, disasters are happening more often, repairs cost more, and insurers have to adjust their rates to keep up. Data from ICE Mortgage Technology helps paint the picture of how the average yearly premium has climbed over the last decade (see graph below):

What You Can Do About It

Homeowner’s insurance is a must to protect your home and your investment. But with costs rising, you’ll want to do your homework to balance the best coverage you can get at the best price possible.

Homeowner’s insurance rates vary widely based on location, provider, and coverage. Shop around and compare quotes before settling on a policy. And don’t forget to ask about discounts. Things like security systems or bundling with auto insurance could help lower your insurance costs.

Bottom Line

When you’re planning to buy a home, it’s important to look beyond just your mortgage payment. You’ll also want to budget for your homeowner’s insurance policy. It gives you a lot of protection against the unexpected. And while it’s true those costs are rising, there are things you can do to try to get the best price possible.

What’s your biggest concern when it comes to budgeting for homeownership? Let’s talk through it and make sure you’re set up for success.

Ground rent is a distinctive characteristic of Maryland real estate law, especially common in Baltimore City and surrounding counties. It involves a homeowner owning the physical structure of a property but not the land beneath it. Instead, the homeowner leases the land from a ground lease holder and pays a recurring ground rent, typically a small, fixed fee paid twice a year, ranging from $50 to $150 annually . This practice, with origins in feudal England, has a long and intricate history in Maryland, dating back to colonial times . This report explores the historical development, evolution, and current status of ground rent in Maryland, including its impact on homeowners and communities.

Origin and Historical Context of Ground Rent in Maryland

The roots of ground rent in Maryland trace back to 1632 when King Charles I of England granted Cecilius Calvert, the second Lord Baltimore, ownership of all the land in present-day Maryland . Calvert collected rents from colonists who settled and built on his land, establishing a system of land leasing that laid the foundation for the modern ground rent system. Following the American Revolution, the Maryland legislature broadened this system, granting any landowner the right to demand rent . In the early days, some landowners accepted alternative forms of payment, such as tobacco or even a single red rose, reflecting the historical significance of these tributes .

Ground rent played a crucial role in Baltimore’s growth as an industrial powerhouse in the early 20th century. It facilitated the development of affordable housing, particularly rows of red-brick rowhouses with their iconic white marble steps. Developers recognized that working-class families could achieve homeownership more easily if they weren’t burdened with the cost of the land. By leasing the land at a minimal cost, developers could use the ground rent payments to generate profits and fuel further construction, expanding affordable housing options in the city .

It’s important to understand the homeowner’s responsibilities in a ground rent arrangement. While they own the house itself, they are also responsible for maintaining the land and any improvements made to it, including the house . This means that homeowners are not only required to pay ground rent but also bear the costs of property upkeep and renovations.

However, the ground rent system has always been a subject of debate. While intended to promote homeownership, concerns arose about developers potentially exploiting the system for profit and the possibility of substandard housing conditions emerging due to the separation of land and structure ownership . This tension between affordability and potential exploitation, particularly its contribution to racial disparities in housing, has been a recurring theme in the history of ground rent in Maryland .

When considering a property purchase in Maryland, it’s essential to understand the distinction between “Fee Simple” and “Ground Rent” listings. “Fee Simple” indicates that the purchase price includes both the house and the land, while “Ground Rent” signifies that the buyer will be required to pay a fee to the landowner .

Evolution of Ground Rent Laws and Regulations in Maryland

Maryland’s ground rent laws have evolved significantly over time, with notable changes occurring in recent decades. The Maryland legislature has taken steps to address concerns about homeowner protection and transparency in ground rent arrangements. Here’s a timeline of key legislative changes:

Post-American Revolution: The Maryland legislature empowered any landowner to demand ground rent, expanding the system beyond the original grants by Lord Baltimore .

1959: Delegate Joseph A. Acker introduced a bill to phase out ground rents by requiring that they be sold along with the homes, although this bill did not become law .

2007: The Maryland General Assembly passed comprehensive legislation aimed at reforming the ground rent system . This legislation introduced several key changes:

Mandatory registration of ground leases: Ground lease holders were required to register their ground rent properties with the State Department of Assessments and Taxation (SDAT) . Initially, failure to register could result in the extinguishment of the ground rent, but this provision was later ruled unconstitutional .

Elimination of ejectment: The law initially sought to eliminate the ground lease holder’s right to eject a homeowner for non-payment of ground rent . However, this provision was later overturned by the Maryland Court of Appeals .

Notice and cure period: Ground lease holders were required to provide homeowners with a 60-day notice and an opportunity to cure any default before taking legal action .

Redemption of irredeemable ground rents: Previously irredeemable ground rents were required to file a notice of intent to preserve irredeemability, or they would become redeemable .

2023: Further legislation was enacted to enhance homeowner protections and simplify the process of redeeming ground rent . These changes included:

Expanded notice requirements: Ground lease holders are now required to use specific forms developed by SDAT when billing for ground rent, demanding payment, or taking legal action . This ensures that homeowners receive clear and consistent information about their rights and obligations.

Clarification of registration: A ground lease is not considered registered until it is posted on the SDAT online registry . This promotes transparency and ensures that homeowners can easily verify the registration status of their ground lease.

Repeal of waiting periods: Certain waiting period requirements for homeowners seeking to redeem their ground rent were repealed . This streamlines the redemption process and makes it easier for homeowners to gain full ownership of their property.

Public interest declaration: The Maryland General Assembly declared that it is in the public interest for ground rents to be redeemed . This statement underscores the legislative intent to phase out ground rent arrangements and promote full homeownership.

These legislative changes reflect a growing trend towards empowering homeowners and phasing out the ground rent system in Maryland.

Potential Impact of Ground Rent on Homeowners and Communities in Maryland

Ground rent can have both advantages and disadvantages for homeowners and communities in Maryland.

Positive Impacts:

Increased affordability: Ground rent can make homeownership more attainable by lowering the upfront purchase price . This can be particularly helpful for first-time homebuyers and those with limited financial means.

Negative Impacts:

Financial burden: Ground rent constitutes an ongoing financial obligation for homeowners, which can pose challenges for those with fixed incomes or facing financial difficulties .

Risk of foreclosure: Failure to pay ground rent can result in legal action, including liens and foreclosure, potentially leading to the loss of the home . To illustrate this risk, consider the case of Deloris McNeil, a Baltimore resident who lost her home of 20 years due to falling behind on ground rent payments .

Complexity and confusion: The ground rent system can be intricate and difficult to navigate, especially for those unfamiliar with its specific rules and regulations . This complexity can lead to misunderstandings and disputes between homeowners and ground lease holders. The opaque nature of ground rent can further disadvantage homeowners and contribute to racialized dispossession .

Racial disparities: Studies indicate that ground rent disproportionately affects Black communities and low-income households in Baltimore, exacerbating racial disparities in wealth and housing security .

Redeeming Ground Rent in Maryland

Homeowners in Maryland generally have the right to redeem their ground rent, which means purchasing the land from the ground lease holder . This allows homeowners to gain full ownership of their property and eliminate the ongoing obligation of ground rent payments.

The process for redeeming ground rent involves notifying the ground lease holder and submitting an application to the State Department of Assessments and Taxation (SDAT), along with the required fee . The redemption amount is calculated based on a formula that considers the annual ground rent and the year the lease was created .

Here’s a table summarizing the capitalization rates used to determine the redemption amount:

Lease Execution Year Range

Capitalization Rate

July 2, 1982 – Present

12%

April 6, 1888 – July 1, 1982

6%

April 8, 1884 – April 5, 1988

4%

Prior to April 9, 1884

Negotiable and possibly non-redeemable

For example, if the annual ground rent is $100 and the lease was established in 1945, the redemption amount would be calculated as $100 divided by 0.06, resulting in $1,666.67. It’s important to note that legal fees and taxes may also apply during the redemption process .

To further assist homeowners, the Maryland General Assembly has created a program that provides loans to eligible homeowners to help them redeem their ground leases . This program aims to make it financially feasible for more homeowners to achieve full ownership of their property.

Significant Legal Cases and Disputes Related to Ground Rent in Maryland

Ground rent in Maryland has been the subject of numerous legal challenges and disputes, often revolving around the respective rights and responsibilities of ground lease holders and homeowners. These legal battles reflect the conflicting interests at play and the ongoing efforts to balance those interests within the framework of Maryland law .

Here are some notable legal cases related to ground rent in Maryland:

Muskin v. State Department of Assessments and Taxation (2011): This case challenged the constitutionality of the 2007 law that sought to extinguish unregistered ground rents. The Maryland Court of Appeals ruled that this provision was unconstitutional because it infringed upon the property rights of ground lease holders without due process or just compensation .

State of Maryland v. Stanley Goldberg, et al. (2014): This case examined the validity of the 2007 law that aimed to eliminate ejectment as a remedy for non-payment of ground rent. The Court of Appeals held that this provision was invalid because it interfered with the ground lease holder’s reversionary interest in the property, which includes the right to reclaim possession if the ground rent is not paid .

Westminster Management v. Smith (2024): This case provided clarity on the definition of “rent” in residential leases, including ground leases. The Supreme Court of Maryland ruled that “rent” refers only to the fixed, periodic payments made for the use and occupancy of the property. Landlords cannot allocate rent payments to cover other obligations, and penalties for late rent payments are limited to 5% of the monthly rent due .

Class action lawsuit in Anne Arundel County: This lawsuit challenges the constitutionality of ground rent reforms, arguing that they have rendered ground rent leases worthless and constitute an unconstitutional taking of private property without just compensation .

These cases illustrate the complexities of ground rent law in Maryland and the ongoing efforts to ensure fairness and balance for both ground lease holders and homeowners.

Current Status of Ground Rent in Maryland

Ground rent remains a legal and relevant aspect of Maryland real estate, primarily concentrated in Baltimore City and some surrounding counties. The state continues to regulate ground rent arrangements, with a strong emphasis on protecting homeowners and ensuring transparency. Recent legislation reflects a clear policy direction towards promoting the redemption of ground rents as a means of phasing out the system .

Here are some key aspects of the current status of ground rent in Maryland:

Registration requirement: Ground lease holders must register their ground rents with SDAT to legally collect payments . This requirement helps ensure that homeowners are aware of their ground rent obligations and can identify the rightful owner of the ground lease.

Redemption rights: Homeowners generally have the right to redeem their ground rent, purchasing the land from the ground lease holder . This allows homeowners to gain full ownership of their property and eliminate the ongoing ground rent payments.

Limited ejectment: While ejectment is still a legal option for non-payment of ground rent, ground lease holders must adhere to strict notice requirements and provide homeowners with an opportunity to cure the default . This protects homeowners from losing their homes without proper notification and a chance to rectify the situation.

Financial assistance: The Maryland General Assembly has established a program to provide loans to eligible homeowners to help them redeem their ground leases . This program aims to make it financially feasible for more homeowners to achieve full ownership of their property.

Irredeemable Ground Rents Registry: All previously irredeemable ground rents became redeemable after April 1, 2023 . This significant change provides homeowners with the opportunity to gain full ownership of their property, even if their ground rent was previously considered irredeemable.

Despite the reforms and legal challenges, ground rent continues to have a significant impact on homeowners and communities in Maryland.

Conclusion

Ground rent in Maryland has a long and intricate history, influenced by legal precedents, legislative reforms, and social and economic factors. While initially intended to promote affordable housing, the system has faced criticism and undergone significant changes over time. The current legal framework strives to balance the interests of ground lease holders and homeowners, with a focus on protecting homeowners from exploitation and promoting transparency. However, ground rent continues to present challenges and raise concerns about its impact on homeowners and communities, particularly in Baltimore City.

Recent legislation in Maryland demonstrates a clear shift towards encouraging the redemption of ground rents and ultimately phasing out the system. This reflects a growing recognition of the potential burdens and complexities associated with ground rent, as well as a commitment to promoting full homeownership and greater equity in housing.

The future of ground rent in Maryland is likely to involve continued debate and potential further reforms. As Maryland addresses issues of housing affordability, equity, and community development, the ground rent system will undoubtedly be a key consideration in shaping housing policy and ensuring fair and sustainable homeownership opportunities for all residents.

Richard Iarossi, REALTOR®

Coldwell Banker Realty

1300 Main Chapel Way, Gambrills, MD 21054

443.995.9595 Cell

410.721.0103 Office

richard.iarossi@cbmove.com

richsellshomes.com

There’s no denying affordability is tough right now. But that doesn’t mean you have to put your plans to buy a home on the back burner. Many buyers can consider purchasing a fixer upper.

If you’re willing to roll up your sleeves (or hire someone who will), buying a house that needs some work could open the door to homeownership. Here’s everything you need to know so you can decide if this is the right move for you.

What’s a Fixer Upper?

A fixer-upper is a home that’s livable but requires some renovations. Think cosmetic updates like wallpaper removal and new flooring or more extensive repairs like replacing a roof or updating plumbing.

While fixer-uppers need a little TLC, here’s why they may be worth considering, especially right now:

They Usually Have a Lower Price Point. Because of the repairs involved, these homes are usually less expensive up front than move-in-ready options. According to a survey from StorageCafe, fixer-uppers come with price tags that are about 29% lower, making them a solid choice if you’re having trouble finding anything in your budget.

Less Competition. When you’re ready to make an offer, you’re less likely to deal with competition from other buyers who are focused on move-in-ready homes.

Build Equity Faster. From choosing how to redo the floors to picking which cabinets you want in the kitchen, a fixer-upper allows you to design a space that fits your needs and style. And with smart renovations, you can increase your home’s value faster and potentially see a big return on your investment.

As The Mortgage Reports notes:

“If you’re a house hunter who’s not afraid of sweat equity, buying a fixer-upper could be your ticket to homeownership. Doing so could lead to big savings, even in some of the nation’s largest and most popular housing markets. Plus, adding the right features could help your investment.”

What To Know About Buying a Fixer-Upper

The possibilities that come with a fixer-upper are exciting, but there are a few things to think about first.

Do You Have a Gameplan? Consider if you have the time, skills, or budget to tackle renovations. Be honest about what you can handle yourself, what you’ll need to hire out, and if a fixer-upper is truly a good fit for your lifestyle. Remember, you’ll likely be living in a construction zone at least for a little while.

Prioritize the Repairs and Upgrades: Don’t stress yourself out thinking you’ve got to do all the work up front. Space out renovations over time in a way that makes sense for your budget and what’s most important to tackle first.

Location Matters: You want the money you’re spending to fix up a house to be worth the investment. So, make sure the home is in an area with increasing home values and amenities locals love, like parks and restaurants.

Get a Home Inspection: Hiring an inspector to do a thorough inspection before you buy is a must. What they find will help you understand what needs to be updated, renovation costs, and if it’s a project you want to take on.

Budget for Surprises: Renovations rarely go as planned. So, be sure to set aside extra money to cover things like extended repair timelines, an increase in the cost of materials, or other unknowns that may come up.

Talk to a Lender About Financing Options: There are some renovation mortgages designed for homes that need a little work. But they may have requirements like spending and timeline limits, so talk to a trusted lender to understand the fine print.

Bottom Line

Fixer-uppers aren’t for everyone, but if you’re open to doing a bit of work, they can be a great way to overcome today’s affordability hurdles and find something in your budget.

With the right mindset and careful planning, you could turn a less-than-perfect house into the perfect home for you.

If you found a fixer-upper that fits your budget and goals, would you consider taking the plunge? If so, let’s connect to explore what’s out there.

Richard Iarossi, REALTOR

Coldwell Banker Realty

1300 Main Chapel Way, Gambrills, MD 21054

443.995.9595 Cell

410-721-0103 Office richsellshomes.com

rich@richsellshomes.com

The 3 Biggest Mistakes Sellers Are Making Right Now

If you want to sell your house, having the right strategies and expectations is key. Don’t make some common seller mistakes. But some sellers haven’t adjusted to where the market is today. They’re not factoring in that there are more homes for sale or that buyers are being more selective with their budgets. And those sellers are making some costly mistakes.

Here’s a quick rundown of the 3 most common missteps sellers are making, and how partnering with an expert agent can help you avoid every single one of them.

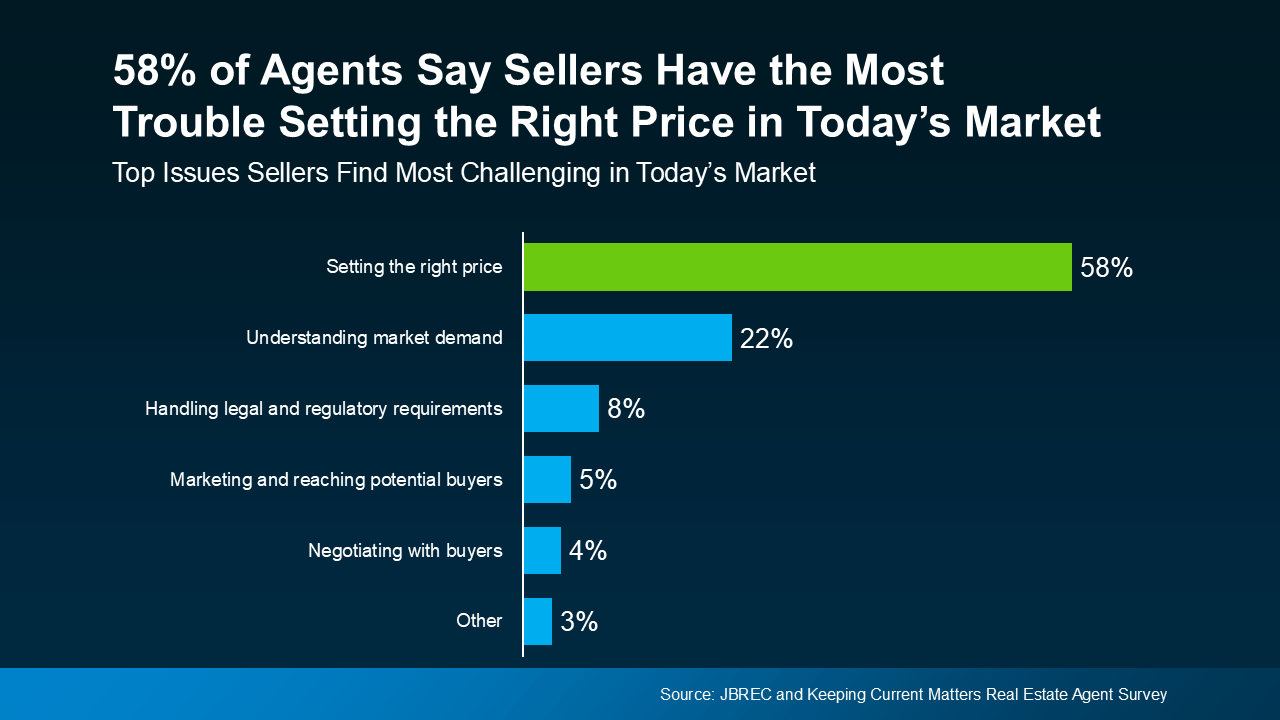

1. Pricing the Home Too High

Of all the seller mistakes, this is the number one. According to a survey by John Burns Real Estate Consulting (JBREC) and Keeping Current Matters (KCM), real estate agents agree the #1 thing sellers struggle with right now is setting the right price for their house (see graph below):

And more often than not, homeowners tend to overprice their listings. If you aren’t up to speed on what’s happening in your local market, you may give in to the temptation to price high so you can have as much wiggle room as possible to negotiate. You don’t want to do this.

Today’s buyers are more cautious due to higher rates and tight budgets, and a price that feels out of reach will scare them off. And if no one’s looking at your house, how’s it going to sell? This is exactly why more sellers are having to do price cuts.

To avoid this headache, trust your agent’s expertise from day 1. A great agent will be able to tell you what your neighbor’s house just sold for and how that impacts the value of your home.

2. Skipping Repairs

Another common mistake is trying to avoid doing work on your house. That leaky faucet or squeaky door might not bother you, but to buyers, small maintenance issues can be red flags. They may assume those little flaws are signs of bigger problems — and it could cost you when offers come in lower or buyers ask for concessions. As Investopedia says:

“Sellers who do not clean and stage their homes throw money down the drain. . . Failing to do these things can reduce your sales price and may also prevent you from getting a sale at all. If you haven’t attended to minor issues, such as a broken doorknob or dripping faucet, a potential buyer may wonder whether the house has larger, costlier issues that haven’t been addressed either.”

The solution? Work with your agent to prioritize anything you’ll need to tackle before the photographer comes in. These minor upgrades can pay off big when it’s time to sell.

3. Refusing To Negotiate

Buyer’s today are feeling the pinch of high home prices and mortgage rates. With affordability that tight, they may come in with an offer that’s lower than you want to see. Don’t take it personally. Instead, focus on the end goal: selling your house. Your agent can help you negotiate confidently without letting emotions cloud your judgment.

At the same time, with more homes on the market, buyers have options — and with that comes more negotiating power. They may ask for repairs, closing cost assistance, or other concessions. Be prepared to have these conversations. Again, lean on your agent to guide you. Sometimes a small compromise can seal the deal without derailing your bottom line. As U.S. NewsReal Estate explains:

“If you’ve received an offer for your house that isn’t quite what you’d hoped it would be, expect to negotiate . . . the only way to come to a successful deal is to make sure the buyer also feels like he or she benefits . . . consider offering to cover some of the buyer’s closing costs or agree to a credit for a minor repair the inspector found.”

The Biggest Mistake of All? Not Using a Real Estate Agent

Notice anything? For each of these mistakes, partnering with an agent helps prevent them from happening in the first place. That makes trying to sell your house without an agent’s help the biggest mistake of all.

Bottom Line

Avoid these common seller mistakes by starting with the right plan — and the right agent. Let’s connect so you don’t fall into any of these traps.

Richard Iarossi, REALTOR

Coldwell Banker Realty

1300 Main Chapel Way

Gambrills, MD 21054

443-995-9595 Cell

410-721-0103 Office

richsellshomes.com

rich@richsellshomes.com

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Of course, moving to a different state isn’t for everyone – and isn’t a necessity. The right agent can help you find more cost-effective options wherever you are.

Of course, moving to a different state isn’t for everyone – and isn’t a necessity. The right agent can help you find more cost-effective options wherever you are.